Review of the Enacted Budget

State Fiscal Year 2021-22

April 2021

Message from the Comptroller

More than a year after the onset of the COVID-19 pandemic in New York, our State continues to recover from the pandemic’s devastation. Fortunately, prospects have improved in recent months. Vaccinations are accelerating, job growth is rebounding, and State and local governments are receiving essential federal aid to provide greatly needed fiscal relief — all positive developments for the enactment of a new State Budget.

The American Rescue Plan (ARP), signed by President Joseph Biden in March, will provide $12.6 billion in direct fiscal relief to New York State, in addition to billions of dollars more in support for New York City and other local governments, school districts, and transit systems. The ARP also provides critical funding for programs to help households and small businesses still struggling with economic losses from the pandemic. This is an appropriate and necessary role for the federal government, and these resources will be critical for helping New Yorkers move forward and for achieving an equitable recovery.

In addition to federal aid, the Enacted Budget for State Fiscal Year 2021-22 relies on substantial new resources from temporary tax increases, including a three-year increase to corporate franchise tax rates and a seven-year increase to personal income tax rates for high-income earners. Together these resources will support the largest budget in State history: $212 billion, or almost 10 percent greater than last year.

While the Enacted Budget makes important investments that are needed now in education, health care and other areas, it is important to also maintain a long-term view and ensure that spending not grow to unsustainable levels. In that regard, the Enacted Budget misses the opportunity to set aside new revenues in the State’s statutory rainy day funds, which will remain at $2.5 billion. Bolstering reserves will be critical to ensuring the State is well-positioned to weather future emergencies and recessions.

Thomas P. DiNapoli

State Comptroller

Table of Contents

I. Executive Summary

The New York State All Funds Budget for State Fiscal Year (SFY) 2021-22 totals an estimated $212 billion — the largest budget in State history, almost 10 percent greater than the prior year.

As the State’s economic recovery continues, tax collections have surpassed expectations and forecasts have improved. In addition, the State will also benefit from a historic amount of federal aid and new revenues from tax increases, the legalization of recreational marijuana, and online sports betting, totaling an estimated $26.7 billion in SFY 2021-22.

The federal government has enacted six relief packages in response to the COVID-19 pandemic, with the most recent, the American Rescue Plan, providing $12.6 billion in fiscal relief to New York State, and additional funds for New York City, school districts, Medicaid, transit systems, and for programs to directly benefit New Yorkers. The State Budget will use $5.5 billion of fiscal aid in SFY 2021-22 and is required to use the remainder by December 2024.

Revenue actions, including increases to top personal income tax rates and corporate franchise tax rates, are expected to generate $3.7 billion in SFY 2021-22, growing to $4.8 billion by SFY 2024-25. Increases to the corporate franchise rates expire after 2023, while the higher personal income tax rates will expire after 2027.

The new resources fund substantial investments in education and programs to relieve struggling New Yorkers and industries. State funding for K-12 public school education is expected to grow by $1.4 billion annually, in addition to federal funding provided directly to school districts. New programs, backed mostly by federal funds, include $2.4 billion for rent and homeowner relief, $2.4 billion for child care resources to aid providers and improve subsidies to low-income parents, and $1.6 billion in small business recovery grants and loans, including specific programs for restaurants, cultural establishments, and theater and musical productions.

Despite the influx of new resources, a number of opportunities to improve the State’s long-term fiscal position were missed. The State continued to defer $3.5 billion in Medicaid payments and did not make any new deposits to statutory rainy day reserve funds, which remain at $2.5 billion. Despite a strong cash position, short-term borrowing was reauthorized. And, for the second consecutive year, State leaders circumvented the State’s statutory cap for debt to be issued in the coming year — with new State borrowing likely to exceed the debt limits, rendering the cap meaningless.

In the coming weeks, the Division of the Budget (DOB) will release an updated four-year Financial Plan for SFY 2021-22 through SFY 2024-25 which will clarify the use and timing of federal aid, spending planned for future years, and the impact of revenue and expense actions on recurring budget gaps. The Financial Plan should also provide detail on several risks, including the volatility and temporary nature of new tax revenues and the sustainability of spending on key programs.

II. Economy and Revenue

State lawmakers enacted a budget for SFY 2020-21 in a highly uncertain environment that included sharply rising case counts of COVID-19 and rapidly mounting job losses. However, with both public health and economic prospects improving over the course of the year, the State passed the SFY 2021-22 Budget with a greatly improved revenue outlook. Federal aid also provided a stabilizing force in SFY 2020-21 and a significant boost for SFY 2021-22; combined with tax increases and other sources, the SFY 2021-22 Enacted Budget includes more than $26.7 billion in new resources.

Economic Downturn: Not as Bad as Initially Forecast

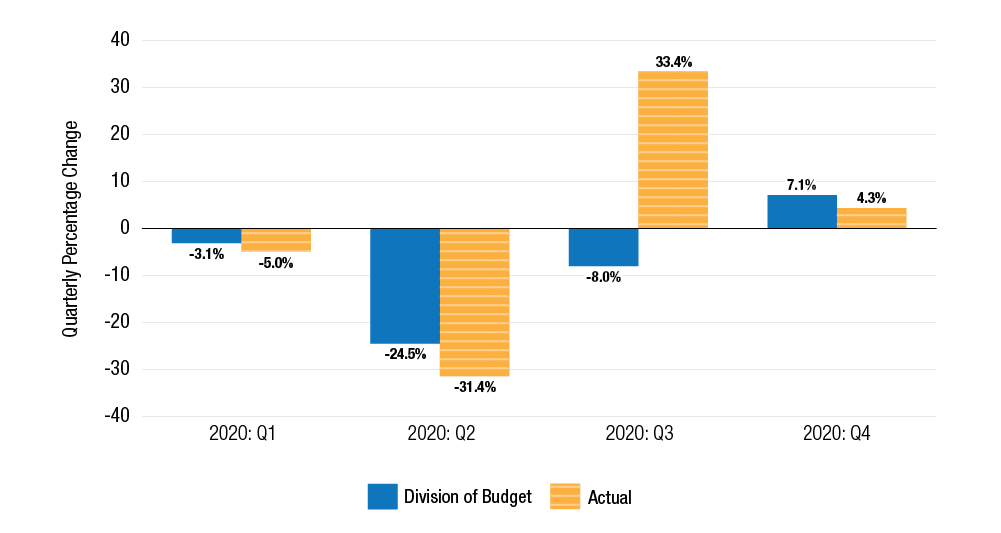

Economic performance for calendar year 2020 outpaced the initial forecast by DOB in the SFY 2020-21 Enacted Budget Financial Plan. DOB projected the national gross domestic product would decline by 5.7 percent, while the actual decline was 3.5 percent. As shown in Figure 1, the DOB forecast underestimated the negative impact of the COVID-19 pandemic in the first half of 2020; however, it also underestimated the timing and strength of the rebound. The national economy grew 33.4 percent in the third quarter of 2020, compared to the initial DOB forecast of a decline of 8.0 percent.

FIGURE 1 – Comparison of U.S. Quarterly 2020 Real GDP Growth, Division of Budget Forecast in April 2020 and Actual Growth

Note: Quarterly percentages at seasonally adjusted, annual rates.

Sources: U.S. Bureau of Economic Analysis; NYS Division of Budget, FY21 Enacted Budget Financial Plan

New York employment declined by 10.3 percent in 2020, more steeply than DOB initially forecast; however, wages declined by less than projected (see Figure 2). Personal income also fared much better than projected, buoyed by the additional unemployment benefits and economic impact payments provided in federal relief packages.

FIGURE 2 – Comparison of New York Economic Indicators, DOB Forecast in April 2020 and Actual Results, Calendar Year 2020

| DOB Projected | Actual | |

| (annual percent change) | ||

| Personal Income | 0.8% | 4.7% |

| Wages | -3.4% | -2.3% |

| Employment | -6.4% | -10.3% |

Sources: U.S. Bureau of Economic Analysis, U.S. Bureau of Labor Statistics, NYS Division of Budget

In addition, after losing, on average, a third of their values in March 2020, the three major stock market indices — the S&P 500, Dow Jones Industrial Average, and Nasdaq — rebounded significantly to end the year at record highs. This strong performance contributed to a 10 percent increase in bonuses paid to securities industry employees.1

Tax Revenue: Bolstered by Strong Personal Income Tax Receipts

Stronger-than-expected economic performance meant that declines in State revenues were not as steep as initially feared. In the SFY 2020-21 Enacted Budget Financial Plan, All Funds tax revenues were estimated to decline by 8.9 percent in SFY 2020-21, and to remain flat in SFY 2021-22. Tax collections were not projected to return to pre-pandemic levels until SFY 2023-24. However, tax collections, particularly for the personal income tax (PIT), consistently outperformed expectations. Tax revenues for SFY 2020-21 totaled $82.4 billion, falling short of the prior fiscal year by only $0.5 billion. Figure 3 compares actual SFY 2020-21 performance by revenue source to the prior year and to final SFY 2020-21 estimates.

FIGURE 3 – Comparison of All Funds Tax Revenues by Tax Category, SFYs 2019‑20 and 2020‑21

(in millions of dollars)

| SFY 2019-20 | SFY 2020-21 | Difference | |||

|---|---|---|---|---|---|

| Executive 30-Day Estimate | Actual | Actual vs. SFY 2019-20 | Actual vs. 30-Day Estimate | ||

| Personal Income Tax | 53,659 | 53,042 | 54,967 | 1,308 | 1,925 |

| Consumption Taxes | 18,022 | 16,001 | 16,118 | (1,904) | 117 |

| Business Taxes | 8,996 | 8,178 | 8,792 | (204) | 614 |

| Other Taxes | 2,212 | 2,125 | 2,499 | 287 | 374 |

| Total Taxes | 82,889 | 79,346 | 82,376 | (513) | 3,030 |

Sources: NYS Division of Budget, SFY 2021-22 Executive Budget as Amended, Office of the State Comptroller.

Federal Aid: Stabilizing Force in SFY 2020-21 and Huge Boost in SFY 2021-2022

The State was allocated historic amounts of federal aid through five major laws crafted in response to the pandemic that DOB estimates will bring $27.1 billion to New York across several fiscal years. These resources were an important stabilizing force to the Budget, staving off the most devastating cuts to vital services. Figure 4 details the most significant aid categories, including Education ($7.1 billion) and enhanced Federal Medicaid Assistance Percentage ($5.6 billion). While most of this funding flows through the State Budget, certain resources do not, including $1.5 billion provided directly to institutions of higher education in the State.

FIGURE 4 – Pandemic Relief to New York: 2020 Federal Legislation (Multiple State Fiscal Years)

(in millions of dollars)

| Education Stabilization Fund | 7,125 |

| CARES | 1,781 |

| CRSSA | 5,344 |

| Enhanced Federal Medicaid Assistance Percentage (eFMAP) | 5,564 |

| Coronavirus Relief Fund (CARES) | 5,136 |

| Labor | 4,265 |

| Epidemiology | 1,478 |

| Housing | 862 |

| CARES | 61 |

| CRSSA (Emergency Rental Assistance Program) | 801 |

| Food | 362 |

| Transportation | 476 |

| CARES | 47 |

| CRSSA | 429 |

| Community Development | 214 |

| Healthcare | 9 |

| Other | 1,640 |

| TOTAL | 27,131 |

Note: CARES is the Coronavirus Aid, Relief, and Economic Security (CARES) Act (became P.L. 116-1360 on March 27, 2020); CRRSA is the Coronavirus Response and Relief Supplemental Appropriations (CRSSA) Act (Divisions M and N of the Consolidated Appropriations Act, 2021, became P.L. 116-260 on December 27, 2020). Labor primarily reflects $4.2 billion in unemployment insurance benefits paid through the Lost Wages Assistance program. Epidemiology represents funding for COVID-19 testing and vaccine preparedness and administration and related programs. Food reflects funding for child nutrition and emergency assistance. Transportation consists of funding for transit and highway programs. Other reflects funding for a range of purposes.

Source: NYS Division of Budget, FY 2022 Executive Budget Briefing Book: Estimated Federal COVID-19 Relief in New York by Programmatic Area & Primary Recipient (table, page 6 of Federal Funding section).

In March 2021, additional aid was approved with the $1.9 trillion American Rescue Plan (ARP). New York State will receive $12.6 billion in fiscal recovery aid; DOB indicates that $5.5 billion will be used in SFY 2021-22. Federal standards require that funds be used to cover costs from March 3, 2021 through December 31, 2024. Additional ARP awards for New York include: $9.4 billion for elementary, secondary and special education; $1.6 billion for home- and community-based services related to the Medicaid matching rate; and $353 million for broadband investment. Funding was also allocated directly to New York City ($5.9 billion), other local governments ($4.9 billion), public transit systems, primarily the Metropolitan Transportation Authority ($6.9 billion), and public and private sector higher education institutions ($2.6 billion).

New Revenue Provisions: Tax Increases, New Resources from Gambling and Marijuana Legalization, and New Tax Credits

The SFY 2021-22 Enacted Budget includes actions that will result in a net revenue increase of $3.65 billion in SFY 2021-22, according to DOB estimates, as shown in Figure 5. The most notable revenue increases are from higher PIT rates imposed on taxpayers with incomes in excess of $1.1 million and increased corporate franchise tax rates.

FIGURE 5 – Enacted Revenue Actions, SFY 2021‑22 Through SFY 2024‑25

(in millions of dollars)

| SFY 2021-22 | SFY 2022-23 | SFY 2023-24 | SFY 2024-25 | |

|---|---|---|---|---|

| Personal Income Tax | 2,753 | 2,864 | 3,025 | 4,050 |

| Increase of Top PIT Rates | 2,753 | 3,251 | 3,439 | 4,472 |

| Deduction for COVID-19 Death Benefits | - | (5) | - | - |

| Extension of Farm Workforce Retention Credit | - | - | (11) | (11) |

| Real Property Tax Credit | - | (382) | (403) | (411) |

| Consumption / Use Taxes | 15 | 110 | 154 | 241 |

| Excise Tax on Adult-Use Cannabis | 20 | 115 | 158 | 245 |

| Extension of Alternative Fuels Tax Exemption | (3) | (4) | (4) | (4) |

| Extension of Sales Tax Exemption on Vending Machine Sales | (2) | (1) | - | - |

| Business Taxes | 774 | 1,083 | 760 | (23) |

| Increase of Corporate Franchise Tax Rates | 750 | 1,073 | 796 | - |

| Decoupling from Federal Opportunity Zones Program | 44 | 62 | 44 | 44 |

| Expansion of Excelsior Jobs Program to Include Child Care Services | - | - | (5) | (5) |

| Increase of Historic Properties Credit for Small Projects | - | - | (5) | (5) |

| Extension of Low Income Housing Tax Credits | - | (8) | (16) | (24) |

| Pandemic Recovery and Restart Program Tax Credits | (20) | (40) | (50) | (25) |

| Extension of Musical and Theater Production Credit | - | (4) | (4) | (8) |

| Miscellaneous Receipts | 106 | 366 | 474 | 502 |

| Mobile Sports Wagering | 99 | 357 | 474 | 493 |

| Allowance of Certain Lottery Game Drawings Twice a Day | 7 | 9 | 9 | 9 |

| All Other Revenue Actions | 2 | 2 | - | 1 |

| TOTAL ALL FUNDS IMPACT OF REVENUE ACTIONS | 3,650 | 4,425 | 4,413 | 4,771 |

Source: NYS Division of Budget

Top Personal Income Tax Rates

Increases to top PIT rates are projected to generate $2.8 billion in SFY 2021-22, growing to $4.5 billion in SFY 2024-25. Top PIT rates will increase from 8.82 percent to as much as 10.9 percent, as shown in Figure 6. The change will be in effect for tax years 2021 through 2027; in 2028 and thereafter, the rate will revert to 8.82 percent.

The new tax rates, combined with the top rate of 3.876 percent in New York City, will result in the highest PIT rate — 14.78 percent — in the nation. The top rate in California, which now will be the nation’s second highest, is 13.3 percent. Top rates in neighboring New Jersey and Connecticut are 10.75 percent and 6.99 percent, respectively.

FIGURE 6 – New Personal Income Tax Brackets

| Tax Rate | Filing Status | Taxable Income | ||

|---|---|---|---|---|

| 9.65% | Single | $1.1 Million - $5 million | ||

| Married, Joint | $2.2 Million - $5 million | |||

| Head of Household | $1.7 Million - $5 million | |||

| 10.30% | All Filers | $5 million - $25 million | ||

| 10.90% | All Filers | Over $25 million | ||

Source: NYS SFY 2021-22 Enacted Budget Revenue Article VII Bill (S.25090-C/A. 3009-C)

Based on preliminary data for taxable income in the 2019 tax year, the new tax rates are estimated to impact just over 60,400 New York personal income taxpayers, less than 1 percent of all taxpayers. Figure 7 shows the approximate number of taxpayers at the new tax rates.

FIGURE 7 – Estimated Number of Affected Taxpayers by Resident Status

| New PIT Rate | Resident | Part-Year / Non-Resident | Total |

|---|---|---|---|

| 9.65% | 20,643 | 21,981 | 42,624 |

| 10.30% | 5,093 | 7,309 | 12,402 |

| 10.90% | 1,874 | 3,501 | 5,375 |

| Total Impacted Taxpayers | 27,610 | 32,791 | 60,401 |

Sources: NYS Department of Taxation and Finance, Office of the State Comptroller analysis

Corporate Franchise Tax Rates

The tax rate for the net income base of the corporate franchise tax will be increased from 6.5 percent to 7.25 percent on businesses with incomes over $5 million. Businesses which determine their tax liability using their capital base (rather than net income or fixed dollar minimum bases) will have their rates increased from 0.025 percent to 0.1875 percent. Small businesses will have a capital base tax rate of 0 percent. Increased tax rates will be in effect for tax years 2021 through 2023. In 2024, the capital tax rate will revert to 0 percent, the tax rate that would have previously been in effect starting in tax year 2021.

Legalization of Adult-Use Cannabis

Legislation legalizing adult-use cannabis includes the imposition of excise taxes at the different levels of the distribution chain:

- 0.5 cents per milligram of THC (tetrahydrocannabinol — the main psychoactive element in cannabis) for cannabis flowers, 0.8 cents per milligram of THC for concentrated cannabis, and 3 cents per milligram of THC for edibles;

- 9 percent on the amount of the retail sale;

- 4 percent on the amount of the retail sale, which will be dedicated to local governments; and

- a biennial registration fee of $600 to be paid by wholesalers.

All excise taxes are imposed upon the retail business. Collections from the taxes and fees (except those from the 4 percent tax, which will be provided to local governments), will be deposited to the Cannabis Revenue Fund. This Fund will be used to pay the costs of various State agencies for the implementation and evaluation of the effectiveness of the cannabis law, with the remainder to be allocated as follows:

- 40 percent to the State Lottery Fund;

- 20 percent to the Drug Treatment and Public Education Fund; and

- 40 percent to Community Grants Reinvestment Fund.

Mobile Sports Wagering

Online sports betting will be authorized through the State’s four commercial casinos as well as eight Native American casinos. Sports betting platform providers will be licensed by the Gaming Commission through a competitive process, and will be required to pay a $25 million one-time licensing fee. While the legislation provides for a minimum of two platform providers, the initial licenses will go to the two highest-scoring applicants. Requests for applications (RFAs) for the gaming licenses are to be issued by July 1, 2021, with the two initial licenses anticipated to be awarded by January 1, 2022.

As part of the license applications, platform providers must include at least four sports wagering operators associated with their platforms. These providers will also be required to pay a $5 million annual fee to the casino that houses the provider’s servers. A tax will be imposed upon the gross gaming revenue from mobile sports wagering. The rate of the tax will be determined through a competitive bidding process, but can be no less than 12 percent. The collections from the tax will be allocated as follows:

- 1 percent of receipts in SFY 2021-22 and $6 million annually thereafter will be deposited to the Commercial Gaming Fund for problem gambling education and treatment.

- 1 percent of receipts in SFY 2021-22 and $5 million annually thereafter will be deposited to the General Fund to be used for a statewide youth sports activities and education grant program to be administered by the Office of Children and Family Services.

An annual report on the impact of mobile sports wagering is required to be completed by the Gaming Commission and the Office of Addiction Services and Supports (OASAS). The cost of the report will be borne by the licensees, to be paid through an assessment by the Gaming Commission.

While DOB has estimated collections from the tax on mobile sports betting to total nearly $500 million when fully implemented, the tax rate associated with these estimates has yet to be determined. Actual revenues may differ significantly once the tax rates are finalized through the process of licensing the platform providers. As detailed in a 2020 Comptroller’s report, the last major expansion of State gambling through the licensing of casinos failed to generate the level of revenues initially projected by casino developers in licensing applications.2

Real Property Tax Relief Credit

The Budget includes several new tax credits, the largest of which is a real property tax relief credit for taxpayers with incomes of less than $250,000 who have paid property taxes on their primary residences in excess of 6 percent of their income. The amount of the credit varies from 14 percent to 5 percent of the excess property taxes paid, depending upon income. However, no credit will be allowed for amounts less than $250 and more than $350. This credit is temporary, effective for tax years 2021 to 2023.

Summary of New Resources

The SFY 2021-22 Enacted Budget was adopted with a historic influx of resources, including federal aid, improved collections from existing tax sources, and tax increases. Figure 8 summarizes the total made available since the most recent update to the State Financial Plan was released with the 30-Day Amendments to the Executive Budget in February 2021. These resources are supporting important investments, but the time-limited nature of the majority of these funds will require careful consideration of recurring spending commitments.

FIGURE 8 – Estimated New Resources in the Enacted Budget, SFY 2021‑22 Through SFY 2024‑25

(in millions of dollars)

| 2021-22 | 2022-23 | 2023-24 | 2024-25 | |

|---|---|---|---|---|

| Additional Receipts(1) | 3,030 | 3,030 | 3,030 | 3,030 |

| New Enacted Tax Revenue Changes | 3,650 | 4,425 | 4,413 | 4,771 |

| American Recovery Plan (ARP) - State Fiscal Recovery Funding(2) | 5,500 | 7,069 | - | - |

| Medicaid Funding(3) | 2,379 | - | - | - |

| ARP Education Funding(4) | 6,068 | 1,124 | 1,124 | 1,124 |

| Other ARP Aid(5) | 6,077 | - | - | - |

| Total New Resources | 26,704 | 15,648 | 8,567 | 8,925 |

(1) Additional receipts in excess of SFY 2021-22 Executive Budget projections for SFY 2020-21 are included as part of future revenue baseline.

(2) Funding allocated in SFY 2021-22 based on DOB press release dated April 6, 2021. Table assumes remainder of ARP funding will be used in SFY 2022-23 based on the SFY 2021-22 Executive Budget Financial Plan (as Amended) to use federal fiscal aid in SFY 2021-22 and SFY 2022-23. Federal legislation does allow for this funding to be used through December 2024.

(3) Includes $750 million from the likely extension of an additional quarter (July through September) of eFMAP funding (resulting from the recent renewal of the public health emergency into July 2021) and $1.629 billion in new appropriated funding for home and community based services.

(4) Includes funding for elementary, secondary and non-public school emergency relief, Individuals with Disabilities Education (IDEA) funding for state grants, and funds for infants, toddlers and preschool. Distributed over life of plan as per section 9-b of Part A of Chapter 56 Laws of 2021. Will require federal action to extend one additional year.

(5) Includes all other funding flowing through the State from the American Recovery Plan.

III. Spending Overview

SFY 2020-21 Year-End Overview

The influx of resources from stronger-than-anticipated tax collections and additional federal assistance allowed the State to end SFY 2020-21 in a significantly better financial position than initially anticipated. The $9.2 billion General Fund closing balance was $216.6 million higher than the previous year, and more than $2.4 billion higher than projected in the SFY 2020-21 Enacted Budget Financial Plan.

The improved resources allowed for a number of positive year-end actions, including:

- $8.2 billion of potential local assistance spending reductions were largely avoided;3

- $4.4 billion of short-term notes issued for cash flow purposes in SFY 2020-21 were repaid;

- $3.1 billion in debt service actions were undertaken, including $2.2 billion used to defease debt early and $974.2 million for debt service prepayments; and

- $918 million in remaining pension amortization payments (with the exception of obligations of the Office of Court Administration) from the period between SFY 2010-11 and SFY 2015-16 were retired to save approximately $67 million in future interest costs.

SFY 2021-22 Budget Makes Significant New Investments: Education, Medicaid, and Aid to New Yorkers and Businesses

Greater tax collections from stronger economic growth, robust federal aid, and new tax increases will support the largest projected budget in State history. Preliminary estimates suggest All Governmental Funds spending will exceed $212 billion, or 9.7 percent more than in SFY 2020-21.4 Spending from State Operating Funds is projected to increase more than 6.6 percent to $111 billion. Some of the growth reflects use of federal resources in SFY 2020-21 to lower State spending and in SFY 2021-22 to supplement State spending.

Education

State Aid

The Enacted Budget includes $29.1 billion in State-funded school aid for the 2021-22 school year (SY), an increase of $3.1 billion, or almost 12 percent. The Budget adds State resources and takes action to separate one-time federal funding from those increases. Total school aid (as detailed on the district-by-district “school aid runs” from the State Education Department) includes:

- $19.8 billion in Foundation Aid, $1.4 billion more than the Executive Budget’s proposal to hold spending flat at $18.4 billion. Legislation released with the Enacted Budget includes a plan to phase in full funding for Foundation Aid over three years.

- $938.6 million for Universal Pre-Kindergarten (UPK), an increase of $142 million from SY 2020-21, including $90 million in new federal funding. A separate $15 million will go to competitive grants for UPK expansion, for a total of $105 million.

- $8.3 billion in other formula-driven aid categories, an increase of almost $400 million. The Enacted Budget omitted the Executive’s proposal to consolidate 11 expense-based aid categories (such as transportation, textbooks and school construction) into a single Services Aid block grant, and to reduce the total funding provided.

The year-to-year growth also reflects restoration of $1.1 billion of State funds that were eliminated in SFY 2020-21 through a “pandemic adjustment” due to the availability of federal funds.

Federal Aid

The school aid runs identify two federal aid sources by district, but separate from the State-funded, annual Formula Aid. The runs treat both as one-time aid sources and specify that they be deemed grants in aid and special funds for tracking purposes:

- $3.85 billion in the Coronavirus Response and Relief Supplemental Appropriations (CRRSA) Act, useable through SY 2022-23.5 (The Executive Budget had treated these as part of SFY 2021-22 aid totals, offsetting a $1.3 billion “local district funding adjustment” (LDFA) reduction to State-funded support for schools.6 )

- $8.2 billion from the ARP, distributed as follows:

- $7.6 billion of Elementary and Secondary School Emergency Relief (ESSER) funding, prioritizing high-poverty districts.

- $630 million reserved for Learning Loss Grants for qualifying districts, intended to support summer learning or enrichment, extended day or year programs, and to target the needs of low-income students, those with disabilities, English Language Learners, and homeless students.

- ARP funds are available for obligation through September 2023 (SY 2023-24), but districts will be required to reserve at least half of these funds for use evenly across the four-year period from SY 2021-22 through SY 2024-25, pending an extension of that deadline.

Medicaid

In the Executive Budget, Medicaid spending had already been projected to grow by $6.6 billion, or 8.2 percent, to $86.2 billion in SFY 2021-22. In light of continued enrollment growth — which reached a record high of nearly 7 million recipients in March 2021 — as well as the Enacted Budget’s rejection of various proposed savings actions, year-over-year Medicaid spending growth is likely to exceed Executive Budget levels.

The Enacted Budget did not adopt many of the Executive’s spending cuts, including proposals to reduce Medicaid provider payments by an additional 1 percent across the board, restrict the ability of doctors to prescribe certain drugs to Medicaid patients (i.e., eliminate “prescriber prevails”) and discontinue State indigent care payments to public hospitals. The Budget also delayed transition of the Medicaid pharmacy benefit from managed care to fee-for-service for two years, and required nursing homes to spend a minimum of 70 percent of revenue on direct resident care, including at least 40 percent of revenue on resident-facing staffing, starting January 1, 2022.

The Enacted Budget also included a $1.6 billion federal Medicaid appropriation made available by a 10-percentage point increase in the federal medical assistance percentage for home and community-based services, or other approved services defined in the ARP. States are required to use these funds to supplement the level of State funds spent on home and community-based services for eligible individuals through programs in effect as of April 1, 2021.

Aid to New Yorkers and Businesses

Housing and Rental Assistance

The Enacted Budget provides a $2.35 billion federal appropriation for emergency rental assistance, as well as $100 million in supplemental State funds for costs exceeding federal funding or for landlords or households with priority populations and incomes exceeding statutory limits. Households must meet certain eligibility criteria, including demonstrated risk of homelessness or housing instability and earnings at or below 80 percent of the area median income. Funding is for certain rental payments or rental and utility arrears accrued on or after March 13, 2020. Rental payments are paid directly to the landlord and utility arrears are paid directly to the utility provider. The program expires on September 30, 2025.

The Budget provides $600 million to the Homeownership Relief and Protection program. The program will provide assistance to homeowners for preventing mortgage deficiencies, defaults, foreclosures, loss of utilities or home energy services, and displacements of homeowners experiencing financial hardship after January 21, 2020. Of the $600 million, up to $20 million will be available each year for 3 years ($60 million total) for the Homeowner Protection program to provide mortgage relief assistance, assistance in applying for loan modifications or other types of loss mitigation, direct representation in court proceedings and settlement conferences, and homeownership counseling.

Child Care

The Enacted Budget provides $2.4 billion in additional federal resources to expand child care access in New York, lower costs to families, and help child care providers recover from the pandemic. The funding includes: up to $1.2 billion to stabilize child care providers currently operating or closed due to the public health emergency; $225 million to supplement existing local, State and federal child care subsidies; $192 million to limit co-pays for families receiving subsidies to no more than 10 percent of their income above the federal poverty level; and $100 million to expand child care capacity in areas of the State with an insufficient supply of available child care. The Budget also increases tax incentives to businesses providing child care services to their employees.

Excluded Workers Fund

The Enacted Budget provides $2.1 billion in General Fund support for payments to “excluded workers” who have suffered a loss of work-related income due to the pandemic and who are not eligible for unemployment insurance benefits or federal assistance payments due to their immigration status or other factors. All applicants for the program must provide proof of identity, State residency, and otherwise meet the eligibility requirements for unemployment during the period from March 27, 2020 until April 2021.

The program provides a benefit of $15,600 (minus $780 in tax withholdings) to eligible excluded workers who can demonstrate work-related eligibility by either proving that they filed a State tax return in any of the last three years or providing other forms of proof as deemed sufficient by the State Department of Labor (DOL). If applicants cannot demonstrate proof of work-related eligibility, the program provides a benefit of $3,200 (minus $160 in tax withholdings). The program pays no benefits to those earning more than $26,208 in the previous 12 months prior to the effective date of the act. Applicants are not required to prove that they are lawfully present in the United States.

The statute requires the State Attorney General, and allows the State Comptroller, to review the implementing regulations developed by the State Labor Commissioner before they are finalized. Any rules and other guidance to implement the program may also be reviewed. The statute further authorizes the State Labor Commissioner to bypass competitive bidding, advertisement of the procurement opportunity and the State Comptroller’s review and approval of contracts to administer the program.

Small Business Relief

The Enacted Budget includes over $1.6 billion for a relief package and $600 million in new federal funding targeted to small businesses suffering from the COVID-19 pandemic, with either the Department of Economic Development (DED) or the Urban Development Corporation (UDC) receiving the majority of the funding and administrative oversight:

- $600 million in new ARP funds to DED for the State Small Business Credit Initiative (SSBCI) to leverage private capital and provide low-interest loans and other investments to small businesses.

- $800 million for a new COVID-19 Pandemic Small Business Recovery Grant Program administered by UDC to support small businesses that do not qualify for relief under the federal SSBCI or other business assistance programs. Eligible costs are for operating expenses like payroll and rent.

- $25 million for a New York Restaurant Resiliency Grant Program to provide grants to restaurants that offer meals or food to people within distressed or underrepresented communities. Regulations and program parameters will be developed by UDC.

- $40 million allocated to the New York State Council on the Arts to provide grants to support the operations of cultural nonprofit organizations that have been impacted by the COVID-19 pandemic. An additional $20 million capital appropriation is also provided for arts and cultural facility improvements.

- $35 million in tax credits through a new Restaurant Return-to-Work Tax Credit Program. The program will allow a small business in the food services sector with a 40 percent or more decrease in either gross receipts or average full-time equivalent employment from 2019 to 2020 to claim a credit equal to $5,000 per full-time equivalent employee re-hired in 2021. Each business can only claim up to $50,000 in credits.

- $100 million for the New York City Musical and Theatrical Production Tax Credit that allows production companies to claim a tax credit equal to 25 percent of their production costs in tax years 2021 to 2023. A production company can claim up to $3 million in credits if the first performance of the production occurs in the first year of the credit program, reduced to $1.5 million if the first performance is in the program’s second year. In order to receive the credits, the production companies must also: participate in a New York State diversity and arts job training program; have a plan to ensure the production is available for low or no cost to low income New Yorkers; and contribute an amount equal to a maximum 50 percent of the amount of the credits received to the New York Council on the Arts’s Cultural Program Fund after tax year 2023.

IV. Missed Opportunities

The State has received historic levels of federal assistance and expects substantial new resources from tax increases in order to make critical investments necessary to facilitate a strong and equitable recovery from the effects of the COVID-19 pandemic. State leaders also took several positive actions, such as defeasing debt and retiring the lingering payments from a prior pension amortization, with multi-year benefits. However, there were also a number of missed opportunities to correct course on some lingering fiscal deficiencies and to end measures that may have been initially reasonable or necessary in the early months of the pandemic, but are no longer warranted by the State’s improving public health and economic outlook.

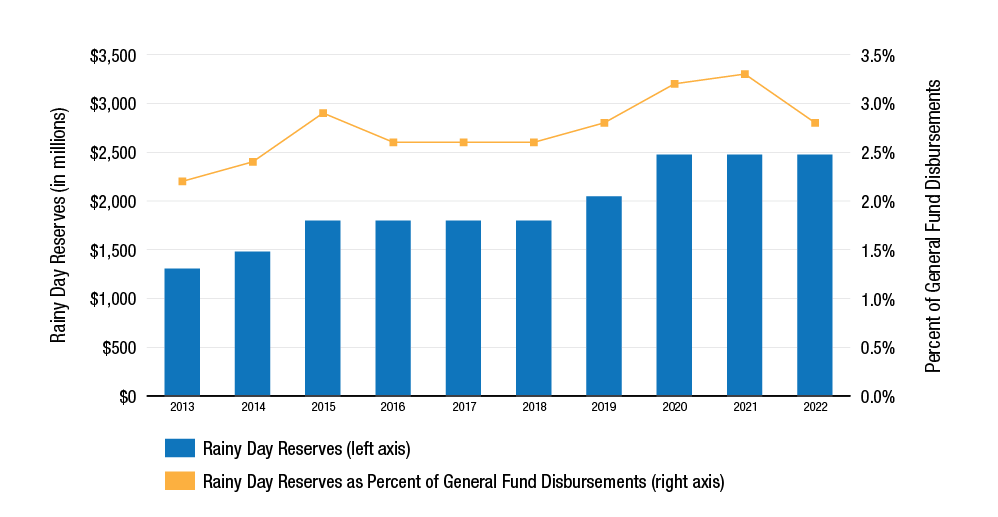

No Additions Made to Rainy Day Reserve Funds

Despite a historic increase in spending, no additional deposits were planned or made to the State’s rainy day funds.7Although current law authorizes a balance of more than $6 billion, the State has just under $2.5 billion in rainy day reserves. While DOB sets aside additional funds in the General Fund for various needs, including economic uncertainties and debt management, the sum of these resources is not high enough to ensure sufficient reserves for future economic downturns.8

FIGURE 9 – Rainy Day Funds, SFY 2012-13 Through SFY 2021-22

Sources: NYS Division of Budget, SFY 2021-22 Executive Budget as Amended, Office of the State Comptroller.

Continued Medicaid Payment Deferral

The State continued to defer $1.7 billion of Medicaid payments ($3.5 billion total including federal share), despite the availability of year-end resources in SFY 2020-21 to make the payment in the fourth quarter. These payment delays provide the appearance that State Department of Health Medicaid spending remains within the “Global Cap,” but obscure true spending on the program.9

Furthermore, the combined impact of deferred payments and enrollment growth will increase pressure on the Financial Plan in subsequent years, particularly in the event of another economic downturn.

Renewed Authorization of Short-Term Borrowing

The Enacted Budget authorizes up to $3 billion in short-term notes and up to $2 billion in letters of credit. Although less than the $11 billion in short-term borrowing enacted in SFY 2020-21, these authorizations are unnecessary given the strength of the State’s cash position and revenue outlook.

Circumventing the Debt Cap

The Enacted Budget again exempts new debt from the provisions of the Debt Reform Act of 2000. The SFY 2020-21 Enacted Budget excluded new debt issued during SFY 2020-21 from the caps on debt outstanding and debt service, as well as the requirement that debt be limited to capital purposes. The SFY 2021-22 Enacted Budget extends those exclusions for new debt issued in the current fiscal year, and allows State-Supported debt for the Metropolitan Transportation Authority to be issued for up to 50 years for bonds issued prior to April 1, 2022. Combined, new debt to be excluded from debt caps and capital requirements could exceed $19 billion.

New authorizations also allow State-Supported debt to refinance up to $1.9 billion of New York City Sales Tax Asset Receivable Corporation (STARC) and Dormitory Authority of the State of New York Secured Hospitals debt, which will also be excluded from the debt caps. The increased level of new debt issuances exceeds what the debt limits are intended to allow, rendering the State’s debt cap functionally meaningless.

Accounting Standards

Many appropriations in the Enacted Budget bills include “refund of appropriation” language which has been interpreted by the Executive to allow certain revenues to refund amounts already spent on an existing appropriation, regardless of the timing of the initial expenditure.10

In certain instances, a credit to the original appropriation is proper; for example, if there has been a refund of a legitimate overpayment within a given program or when a rebate is offered for a pharmaceutical purchased through the Medicaid program. However, the widely expanded use of this language has no dollar limit, and has the potential to result in actual spending beyond amounts set forth in the appropriation for a given fiscal year. Left unchecked, this could also artificially reduce the appearance of true liabilities and reported receipts and disbursements of the State.

Transparency and Oversight Concerns

Certain elements of the Enacted Budget fall short with respect to high standards of transparency, accountability and oversight, undermining the State’s responsibility to promote an accurate understanding of how public resources are generated and spent.

Federal Funds

The Enacted Budget includes a new appropriation for $25 billion that is unnecessarily opaque with respect to how the State would use this appropriation as well as $16 billion that is continued from SFY 2020-21. This may leave the allocation of such extraordinary funds almost entirely at Executive discretion.

Procurement Integrity

The Enacted Budget includes provisions authorizing substantial State spending without standard protections such as requirements for competitive bidding and State Comptroller review and approval of contracts before they become effective, thereby removing important deterrents to waste, fraud and abuse. These provisions include:

- $1.6 billion in increased federal Medicaid funding for home and community-based services permits DOH or the heads of other “sub-allocated” agencies to make grants that are not advertised, competitively awarded or subject to the Comptroller’s pre-approval of contracts.

- Special emergency funding eliminates the State Comptroller’s oversight and waives competitive bidding procedures, including $2 billion to meet emergency and unanticipated expenditures of the State and another $6 billion for services and expenses related to the COVID-19 outbreak.

- The Budget extends until 2026 authority for State and City University of New York (SUNY) and (CUNY) colleges, SUNY hospitals, and SUNY and CUNY Construction Funds to enter into certain contracts without the review and approval of the State Comptroller.

- The New York State Energy Research and Development Authority (NYSERDA) is authorized to use single purpose project holding companies to acquire, sell and transfer rights in build-ready sites. Such holding companies are not considered NYSERDA subsidiaries, thus bypassing important Public Authorities Law reporting requirements.

- The newly-created Excluded Worker Fund authorizes DOL to bypass competitive bidding, advertisement of the procurement opportunity and State Comptroller’s review and approval for non-competitive contracts entered into to administer the program.

- Other exemptions from the State Comptroller’s contract review authority and competitive bidding procedures include over $130 million for the Office of Addiction Services and Supports for substance abuse treatment and prevention programs, and over $100 million for capital projects; and renewal of Division of Housing and Community Renewal contracts with service providers without competitive bidding.

V. Risks for the Future

In coming weeks, DOB will release an updated Financial Plan for SFY 2021-22 through SFY 2024-25, which will clarify use and timing of federal aid, spending planned for future years, and the impact of revenue and expense actions on recurring budget gaps. The Financial Plan should also provide detail on several risks, including the volatility and temporary nature of new tax revenues and the sustainability of spending on key programs.

Increased Revenue Volatility

According to 2019 PIT data, new PIT tax rates will impact less than 1 percent of the State’s personal income taxpayers; however, these taxpayers account for nearly 32 percent of total PIT liability. The income of these taxpayers tends to be very volatile, as it is more dependent on unearned income — such as dividends and capital gains — which can fluctuate considerably from year to year. In addition, some taxpayers have the ability to determine when such income will be realized. This occurred in 2013 when the Bush-era tax cuts expired, and in 2018 when the federal Tax Cuts and Jobs Act was enacted; in these cases, taxpayers delayed or expedited certain income in order to avoid higher tax rates.

The increases to the top PIT rates will result in New York State having the third highest State tax rates in the country; combining these rates with the top New York City PIT rate, New York will be rank first. With the prospect of a higher tax burden, high-income taxpayers may consider relocating. According to Tax Department data, there has been a net out-migration of taxpayers at all income levels over the past five years; however, a larger share of high-income taxpayers have left the State.11 Since the Financial Plan will be even more dependent on high earning taxpayers, it will only require an additional small number of these taxpayers to relocate to adversely impact revenue projections. This risk is also inherent with certain business owners, who will see their corporate taxes increase.

Temporary Resources

While increased receipts will occur from the legalization of marijuana and sports betting, the new revenue sources with the greatest fiscal impacts are the PIT and corporate tax increases, both of which are temporary: new corporate franchise tax rates are in effect until the end of 2023, while higher PIT rates are in effect through 2027. This means that either the higher rates will have to be extended (as previously occurred with the current PIT rate of 8.82 percent), replaced with another revenue source of equal or higher value, or the spending supported by those expiring revenues will need to be reduced.

Sustainability of Spending on Key State Programs

Much of the new spending in SFY 2021-22 is backed by federal dollars; the need for these programs, which are mostly to help struggling New Yorkers and businesses, should wane as federal dollars are used and the economy continues to recover. On the other hand, substantial increases in other programs, such as Education and Medicaid, may be recurring, with significant growth rates projected throughout the life of Financial Plan. It is unclear whether new resources in the Budget will sustain this new spending trajectory.

1 For more on the significance of the securities industry to New York, see Office of the State Comptroller, “2020 Wall Street Bonuses,” March 2021, available at www.osc.state.ny.us/press/releases/2021/03/nys-comptroller-dinapoli-wall-streets-2020-bonuses-rose-amid-volatility.

2 Office of the State Comptroller, “A Question of Balance: Gaming Revenues and Problem Gambling in New York State,” November 2020, available at www.osc.state.ny.us/files/reports/special-topics/pdf/gaming-report.pdf.

3 At this time, DOB has not indicated whether the 5 percent withholding that remains from certain local aid payments in SFY 2020-21 will be paid.

4 Preliminary projections provided by the New York State Assembly Ways and Means committee.

5 Funds are available to be obligated by September 30, 2022, which is in SY 2022-23.

6 For more details, see Office of the State Comptroller, "Report on the State Fiscal Year 2021-22 Executive Budget as Amended by the Governor," March 2021, pp. 34-35, available at: www.osc.state.ny.us/files/reports/budget/pdf/executive-budget-report-2021-22.pdf.

7 Rainy day fund reserves consist of the Tax Stabilization Reserve Fund (TSRF) and the Rainy Day Reserve Fund (RDRF). The maximum balance of the TSRF is 2 percent of the General Fund spending in the current year. The maximum balance of the RDRF is 5 percent of projected General Fund spending in the immediately following fiscal year.

8 For more information, see Office of the New York State Comptroller, “The Case for Building New York State’s Rainy Day Reserves,” December 2019, available at www.osc.state.ny.us/files/reports/budget/pdf/rainy-day-reserves-2019.pdf.

9 Since enactment of the SFY 2011-12 Budget, the State has statutorily limited certain Department of Health spending, primarily in Medicaid. Starting April 1, 2012, such spending has been limited to a percentage based on the medical component of the Consumer Price Index, a limitation known as the indexed portion of the Medicaid Global Cap. Enacted Budgets and administrative actions since then have moved certain elements of the Medicaid program into or out of the Cap — and at times have reversed such shifts with regard to similar expenses.

10 See the Office of the State Comptroller’s "Report on the State Fiscal Year 2020-21 Executive Budget," February 2020 and "Report on the State Fiscal Year 2021-22 Executive Budget (as amended by Gov.)," March 2021, available at https://www.osc.state.ny.us/files/reports/budget/pdf/executive-budget-report-2021-22.pdf. The appropriation language referenced authorizes spending in numerous instances in “an amount net of refunds, rebates, reimbursements, credits, repayments, and/or disallowances.” Moreover, header language in both the Aid to Localities and State Operations budget bills include language broadly defining these terms and directs the Comptroller to credit the original appropriation and “reduce expenditures in the year which such credit is received regardless of the timing of the initial expenditure” (emphasis added).

11 NYS Department of Taxation and Finance Personal Income Tax Study File.