The Retail Sector in New York City

Recent Trends and the Impact of COVID-19

December 2020

Highlights

- In 2019, New York City’s retail sector comprised 32,600 businesses that provided 344,600 jobs, paid $16 billion in total wages citywide, and contributed $55 billion in taxable sales to the City’s economy.

- Taxable sales in retail trade declined by nearly one-third from March to May 2020 compared to one year earlier, with all subsectors posting declines except, notably, nonstore retailers.

- Nonstore retailers, including online retailers, have experienced the most growth in taxable sales of any subsector during the pandemic. Nonstore retailers’ 10-year trend of pre-pandemic job growth exceeded 110 percent.

- By August 2020, employment in essential stores, such as groceries and pharmacies, had returned to pre-pandemic levels while most other retail subsectors, such as clothing and clothing accessories stores, remained below levels from one year earlier.

- Manhattan had nearly half of all the City’s retail jobs in 2019, and these paid an average salary of $59,400, above the citywide average of $46,600. In 2019, 214,600 City residents worked in the retail sector.

- Federal Paycheck Protection Program loans supported half of all small-business retailers and more than one-third of all retail jobs.

- The City is implementing an Open Storefronts program through December 31 to allow retailers to use sidewalks and open spaces.

New York City is one of the world’s premier shopping destinations, topping “best of” lists and drawing visitors from across the globe. The retail sector is a vital part of New York City’s economic and social landscape, with businesses ranging from corner grocery stores to renowned department stores in locations across the City, from neighborhood commercial areas to Manhattan’s major retail corridors.

Retail accounts for 12 percent of businesses and nearly 9 percent of private sector jobs in New York City, and generates sales tax revenues for the State, the City and the Metropolitan Transportation Authority.

The COVID-19 pandemic has affected the retail trade sector unevenly, with online retailers and some essential businesses experiencing growth and other large retail segments seeing falling revenues. The impact has been most obvious in Manhattan, where foot traffic in key corridors initially fell by more than 90 percent and remains below 50 percent of its 2019 levels as tourists, commuters, office workers and residents have responded to pandemic-related shutdowns and public health concerns.

Estimates of potential permanent closures of retail firms are scarce thus far, but data on economic activity in certain subsectors, commercial rental vacancy rates in major corridors, and recent high-profile bankruptcies suggest that segments of the industry face significant challenges from reduced demand and changing consumer behavior. Industry challenges will intensify if the pandemic worsens and more restrictions must be put into place. In order to help the retail industry manage a sustained reduction in economic activity, additional federal relief must augment City and State actions.

Uneven Impacts, Evolving Responses

Along with changes already underway over the past decade, behavioral changes since the pandemic began have generated shifts in retail activity. Demand has increased for certain goods such as food and beverages, and decreased for other goods such as clothing. As people seek to avoid virus transmission, online shopping has expanded relative to purchases at brick-and-mortar stores.

While some essential stores, such as pharmacies and grocery stores, have remained open since the start of the pandemic, many brick-and-mortar retail establishments (categorized as nonessential businesses) have shut or faced operational limitations for months.

Efforts have been made at the City, State and federal levels to help retail stores survive the pandemic. In March, Governor Cuomo issued an executive order that instituted a moratorium on evictions and foreclosures for commercial enterprises. The moratorium has been extended several times, most recently on October 20, and now runs through January 1, 2021. Federal relief has been provided mainly through small-business support programs, including the Paycheck Protection Program.

Business owners have expressed concern about their ability to pay back rent since revenues have dried up. To address this concern, proposals in the State Legislature would lower rent payments for small businesses that have been forced to close or have lost substantial income.1 Proposals also call for the establishment of a commercial rent relief program funded by resources from the federal government, allowing landlords to recoup some unpaid rent.

To encourage shopping during the holiday season, Mayor de Blasio recently announced the Open Storefronts program, which allows most retail store owners to use the sidewalk space in front of their storefronts to display and sell merchandise.2 Stores may also use street space if their street closes to traffic through participation in the Open Streets: Restaurants program. The program runs from October 30 to December 31.

The retail sector is likely to be further affected by efforts to minimize the spread of the virus, in light of the recent surge in infection and hospitalization rates. Measures have included a “microcluster strategy,” under which red zones were delineated around clusters of positive cases. Nonessential businesses in these zones were required to close for a minimum of two weeks. A more recent strategy involves a greater focus on hospitalization rates and implementing restrictions by type of business or larger geographic regions (e.g. borough, citywide).

Retail Sector Profile

The Retail Picture in 2019

Before the pandemic, the retail sector in New York City accounted for 32,600 establishments, 344,600 private sector jobs and $16 billion in total wages in 2019.3 The sector provided about one in 11 private sector jobs (8.8 percent) and encompassed one in eight businesses (12.0 percent). Nationally, the sector represented a higher share of jobs (12.3 percent) and a lower share of businesses (10.5 percent).

Retail corridors, both big and small, service neighborhoods throughout the City. Most retail businesses are small, as 65 percent had fewer than five employees and 90 percent had fewer than 20 employees. Less than 1 percent of all retail firms had 250 or more employees in 2019.

The average salary for retail jobs citywide was $46,600 in 2019, with a much higher salary in Manhattan ($59,400) than in the other boroughs, where the average retail salary ranged between $33,500 and $37,000.

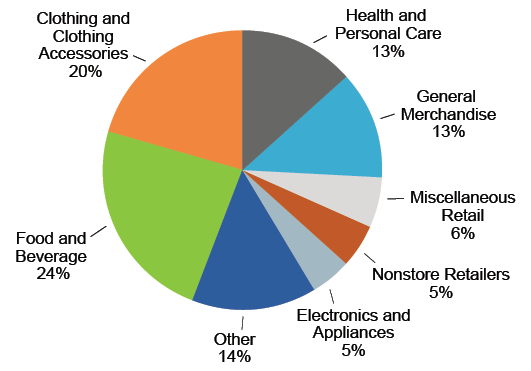

The retail sector includes many different types of stores, such as grocery stores, clothing stores, department stores and pharmacies, which are grouped into major subsectors (see Figure 1).

In 2019, food and beverage stores accounted for more employment than any other subsector (nearly one in four retail jobs citywide). Clothing and clothing accessories stores (which include shoe, jewelry, discount and high-end clothing stores) had the second-highest employment, with one in five retail jobs. These were followed by the health and personal care subsector, including pharmacies; and general merchandise, such as discount stores, department stores and warehouse clubs. Together, these four subsectors accounted for 70 percent of all retail jobs in the City.

FIGURE 1 - Subsector Shares of NYC Retail Employment, 2019

Sources: NYS Department of Labor; OSC analysis

Retail Trends Prior to the Pandemic

From 2009 to 2019, retail employment in the City grew by 19.7 percent, more slowly than total private sector employment (30 percent). Most of the growth occurred prior to 2015, similar to the national trend, after the Great Recession.

Significant restructuring in the retail sector was already underway in the years prior to the pandemic, as various trends intersected. An expansion in online shopping was one of the most significant trends, with widespread impacts on the retail landscape.

As consumers shifted their purchases to online retailers, sales at many chain stores nationwide suffered, forcing some into bankruptcy with resultant store closures. For more than 10 years, the Center for an Urban Future has been following the number of national chain store locations in New York City. Its latest annual report (from 2019) noted declines in the last two years, with a drop of 3.7 percent in 2019. While food retailers and some nonretailers (e.g., gyms) were included in the calculations, the report emphasized a major reduction of merchandise retail locations (such as apparel and cosmetics), some of which were the result of bankruptcies.

Bankruptcies among retailers have continued during the pandemic, with such locally well-known stores as Century 21 and Modell’s Sporting Goods entering proceedings. Some of these retailers will pare down the number of their locations while others will close completely.

Other changes in consumer spending habits also occurred prior to the pandemic. Some consumers shifted discretionary spending toward travel and dining out rather than purchasing goods such as clothing, and some consumers sought greater bargains (moving away from higher-priced brands) during and after the Great Recession.

FIGURE 2 - New York City Retail Employment by Subsector

| Category of Retailers | 2019 Jobs (000s) | Average Salary ($) | Percent Change | |

| 2009-2015 | 2015-2019 | |||

| Food and Beverage | 81.7 | 30,800 | 27% | 0% |

| Clothing and Accessories | 70.3 | 48,200 | 10% | -5% |

| Health and Personal Care | 46.2 | 52,300 | 24% | 3% |

| General Merchandise | 43.3 | 35,500 | 36% | 2% |

| Miscellaneous Retailers | 20.0 | 65,900 | 14% | -1% |

| Nonstore Retailers | 17.1 | 88,400 | 72% | 24% |

| Electronics and Appliances | 16.8 | 59,300 | 27% | -8% |

| Building Material & Garden Equipment | 14.0 | 45,800 | 8% | 2% |

| Motor Vehicle and Parts Dealers | 11.4 | 66,900 | 8% | 7% |

| Furniture and Home Furnishings | 10.5 | 51,100 | 11% | -1% |

| Sporting Goods, Music and Books | 9.7 | 31,900 | -1% | -23% |

| Gasoline Stations | 3.6 | 30,700 | -2% | 17% |

| Total Retail | 344.6 | 46,600 | 21% | -1% |

Sources: NYS Department of Labor; OSC analysis

This retail restructuring impacted employment growth differently depending on the subsector over the past decade (see Figure 2). Employment at food and beverage stores, which grew significantly through 2015 and then leveled off, accounted for nearly one out of every three new retail jobs since 2009. Employment in the nonstore subsector, whose largest component is online retailers at 86 percent of subsector employment, more than doubled, increasing by 114 percent (the fastest growth rate of any retail subsector).

Employment increased at clothing and clothing accessories stores until 2013, when the subsector was no longer the largest, and has declined every year since. The subsector ended 2019 with fewer jobs than in 2010. Nearly two-thirds of jobs in the subsector were located in Manhattan.

Average salaries vary significantly across the retail sectors. Nonstore retailers, which include online retailers, had the highest average salary in 2019, at $88,400; food and beverage stores, gas stations, sporting goods, music and book stores, and general merchandise stores had the lowest average salaries (all below $36,000, compared to $46,600 for retail trade as a whole).

Where Retail Firms Are Located

Manhattan had the largest retail employment among the boroughs, with nearly 157,000 retail jobs in 2019. This represented nearly half (46 percent) of all retail employment citywide. Brooklyn was second with 77,200 retail jobs, followed by Queens with 63,200 jobs, the Bronx with 31,000 jobs and Staten Island with 16,200 jobs.

Retail establishments made up 20.5 percent of businesses in the Bronx, and accounted for 15.5 percent of employment in Staten Island. These were the highest shares among the five boroughs, and much higher than national averages.

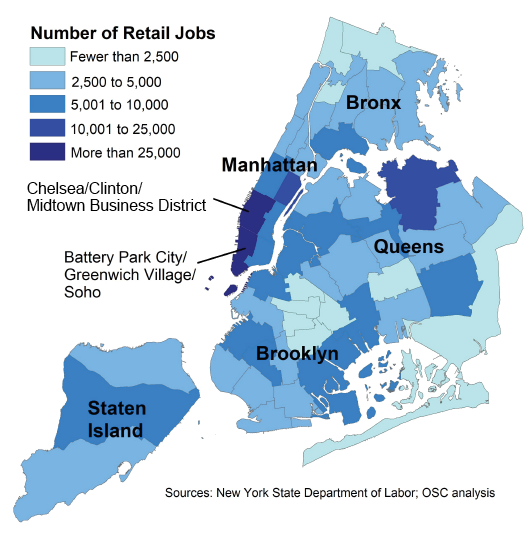

The Chelsea/Clinton/Midtown Manhattan Business District had the largest concentration of retail jobs among the City’s 55 Census-defined neighborhoods, with more than 68,000 retail jobs in 2019.4 Nearly one in five retail jobs citywide, or 19.7 percent of all retail employment, was located in this area (see Figure 3). The Battery Park City/Greenwich Village/Soho neighborhood had the second-largest concentration, with nearly 30,000 retail jobs or 8.6 percent of the citywide total. Together these two neighborhoods accounted for nearly 30 percent of all retail employment citywide.

Still, while the bulk of employment is in Manhattan, local reliance on retail jobs is evident in the share of employment among other neighborhoods across the City. Retail employment accounted for 6.6 percent of total employment in the top two retail neighborhoods in Manhattan in 2019.

However, nearly 80 percent of all other City neighborhoods employed a higher share than the citywide average (8.8 percent). In five neighborhoods (all in the Bronx, Queens and Brooklyn), retail jobs made up more than 20 percent of neighborhood employment in 2019.

FIGURE 3 - NYC Retail Sector Jobs by Neighborhood

In most neighborhoods citywide (42 out of 55), food and beverage stores accounted for the highest share of retail employment, ranging from between 25 percent and 50 percent of all retail employment in each area. For the three Manhattan neighborhoods with the most retail employment, however, the highest shares came from clothing and clothing accessories stores, which made up between 28 percent and 37 percent of retail jobs in those areas.

Retail Work Force

Where Retail Workers Live

In 2019, 214,600 residents (both employed and self-employed) worked either part-time or full-time in the retail sector, with average annual earnings of nearly $40,000. Additional employees commuted from surrounding areas to work in the City’s retail sector.5

The neighborhood where the largest number of retail employees resided was Jamaica/Hollis/ St. Albans (7,900), and the neighborhood where retail workers made up the highest share of the local work force was Belmont/Crotona Park East/East Tremont, at 10.8 percent (see Appendix A). The 10 neighborhoods with the highest numbers of residents working in the retail sector accounted for nearly one-third of all the City’s resident retail workers.

Retail Workers: Demographics

About 44 percent of all retail workers who lived in the City in 2019 were immigrants, similar to their share among all occupations citywide. These shares varied significantly across neighborhoods, however. In 19 neighborhoods, immigrants constituted more than half of retail workers, with shares rising as high as 74 percent (see Appendix A for more detail).

FIGURE 4 - Share of Workers by Race and Ethnicity

| Race/Ethnicity | Retail Workers | All NYC Workers |

|---|---|---|

| Hispanic or Latino | 31% | 27% |

| White | 25% | 35% |

| Black or African American | 22% | 20% |

| Asian | 19% | 15% |

| Other | 3% | 3% |

| Total | 100% | 100% |

Sources: U.S. Census Bureau, American Community Survey, 2019 1-year estimates; OSC analysis

Including both immigrants and native-born residents, Hispanics made up the largest share of retail workers (31 percent) among the total City work force in 2019 (see Figure 4). Blacks or African Americans also represented a higher share of retail workers than among all occupations citywide, as did Asian workers. In contrast, Whites represented a much lower share (10 percentage points) of retail workers than among all workers citywide.

COVID-19 Impact: Then and Now

Impact on Employment

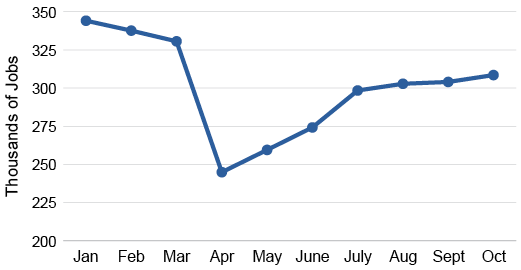

In February 2020, nearly 338,000 people were working in New York City’s retail industry, a slight decline from February levels in the prior two years based on data from the New York State Department of Labor’s Current Employment Statistics.6

FIGURE 5 - New York City Retail Employment, 2020

Sources: NYS Department of Labor; OSC analysis

By March 22, when Governor Cuomo’s statewide stay-at-home order went into effect, the City essentially shut down, causing the closure of many retail establishments. While there was a small decline in employment in March, by April employment had dropped to 245,000 positions (see Figure 5). As the City reopened and progressed from Phase 1 (June 8) to Phase 4 (July 20), employment grew, reaching nearly 309,000 jobs by October. The total number of jobs has changed little since July.

Not all retail establishments closed in March, since grocery stores (including all food, beverage and liquor stores), pharmacies and convenience stores were considered “essential” retail and were allowed to remain open for in-store purchases. Without this, employment declines would likely have been much more severe in these subsectors. Nonetheless, residents were advised to stay at home if possible, and many turned to online and delivery services.

In Phase 1 of the reopening (beginning June 8), most other retail stores were allowed to reopen for delivery, curbside and in-store pickup. In-store retail shopping, with a maximum capacity of 50 percent, was allowed in Phase 2 (June 22), and malls in the City reopened on September 9 with a 50 percent capacity limit.

Reduced in-person patronage has hurt revenues at certain retail stores during the pandemic. Foot traffic data indicates a severe drop in commuters and tourists entering the City, leaving retailers with fewer sales opportunities.

The City has not updated its biannual pedestrian counts on its OpenData portal in 2020. However, the Times Square Business Improvement District has released foot traffic figures in each month since the pandemic began. In April, at the height of the shutdowns, foot traffic dropped by more than 90 percent compared to the same month the year before. September figures show that foot traffic in the neighborhood remains down more than 60 percent compared to a year earlier.

Similarly, data from a number of private firms, including SnapGraph and Foursquare, also show that as of September, foot traffic in 2020 was less than half the rate posted in 2019 in various commercial districts in the Manhattan Central Business District. Current projections from Tourism Economics anticipate that international overnight visits will not return to pre-pandemic levels until 2025, although this will likely hinge on a vaccine. Until a vaccine has been widely distributed and commuters and tourists have returned, a lack of foot traffic is likely to continue and exert downward pressure on revenues for segments of the industry.

Subsector Employment Changes

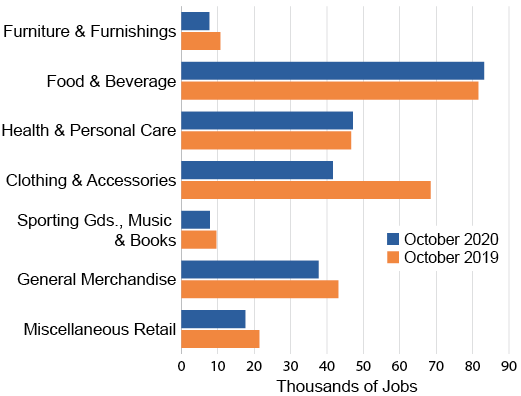

The recovery in retail employment has been uneven. Although employment at clothing and clothing accessories stores increased to 41,600 jobs in October from a low of 28,600 in May, it was still nearly 40 percent below the level of one year earlier (see Figure 6).

Conversely, employment levels at food and beverage stores, and pharmacies and drug stores were slightly higher in October 2020 than in October 2019.

FIGURE 6 - New York City Retail Employment by Subsector, October 2019 vs. October 2020

Sources: NYS Department of Labor; OSC analysis

Taxable Sales

Although there is little actual revenue data currently available, taxable sales reported by vendors to the New York State Department of Taxation and Finance give an indication of revenue trends. Taxable sales also provide the base for State and City sales tax revenues. Retail made up 30.4 percent of all City taxable sales in 2019. As illustrated in Figure 7, taxable sales in retail trade declined by nearly one-third from March to May 2020 compared to one year earlier, with all subsectors posting declines except, notably, nonstore retailers.

During the second quarter of the year (June to August) the decline eased significantly, with taxable sales just 4.6 percent below the second quarter of 2019, and improvements recorded in all retail trade subsectors. Increased online sales contributed, in part, to the growth in taxable sales in the nonstore subsector. In fact, according to the U.S. Census Bureau’s Small Business Pulse Survey, a higher proportion of retail respondents indicated plans to develop online sales or websites over the next six months than respondents in all other sectors.

FIGURE 7 - Change in Taxable Sales by Retail Subsector, 2019 to 2020

| Category of Retailers | Percent Change | |

| Mar-May 2020 | Jun-Aug 2020 | |

| Motor Vehicle and Parts Dealers | -47.1% | 16.6% |

| Furniture and Home Furnishings | -43.2% | -13.2% |

| Electronics and Appliances | -47.4% | -20,7% |

| Building Material & Garden Equip. | -27.8% | 3.2% |

| Food and Beverage | -13.0% | -12.0% |

| Health and Personal Care | -35.7% | -31.0% |

| Gasoline Stations | -48.1% | -30.6% |

| Clothing and Clothing Accessories | -72.8% | -49.5% |

| Sporting Goods, Music, and Books | -33.8% | -16.0% |

| General Merchandise | -32.3% | -12.2% |

| Miscellaneous Retailers | -58.0% | -22.9% |

| Nonstore Retailers | 61.7% | 80.0% |

| Total Retail | -31.8% | -4.6% |

Note: Percent change is from the same period in 2019.

Sources: NYS Department of Taxation and Finance; OSC analysis

Online retailers in other states were required to remit sales taxes beginning June 30, 2019. As a result, as sales from these retailers began to be included, growth in taxable sales for nonstore retailers was up 82.9 percent in the six-month period from September 2019 through February 2020 (prior to the pandemic) compared to the same period a year earlier. The pandemic has accelerated the use of electronic shopping, with the six-month period from March through August 2020 experiencing growth in taxable sales of 105.9 percent.7 Prior to these changes, between 2014 and 2018, average annual growth in taxable online sales was 11 percent. Online retailers’ share of retail taxable sales has also grown, from 14.2 percent in the six-month period prior to the pandemic to 21.6 percent in the six-month period since March 2020.

Taxable sales at food and beverage stores do not include sales of most food items in New York City.8 Womply, a software services company that tracks credit card transactions from hundreds of millions of cardholders, estimates that average daily revenue at grocery stores that remained open increased by nearly 40 percent between January 1 and October 9, 2020, compared to the same period one year earlier.

Household Spending Shifts

Early in the pandemic, the U.S. Census Bureau began the Household Pulse Survey to gather data “on the social and economic effects of coronavirus on American households.” Biweekly survey data for the period from August 19 to October 12, 2020, showed shifts in spending patterns resulting from the pandemic. On average, more than one in five respondents in the New York City metropolitan area (including the 23 counties surrounding New York City) indicated that their normal shopping locations were closed or had limited hours, and an average of nearly half were concerned about health risks associated with going out in public. An average of 47 percent of respondents increased their levels of online spending, and 36 percent increased the use of credit cards and smartphone apps to make purchases.

Retail Operations

With the falloff in revenues, many retail stores were not able to remain open. As of October 18, Womply estimated that one-quarter of retail and wholesale establishments in New York City had closed since March 1, 2020 (given Womply’s methodology, some of the reported closures may be temporary).

FIGURE 8 - PPP Retail Sector Loans and Jobs Reported as Share of Small Business Firms and Jobs

| Borough | Retail Firms | Employment by Retail Firms | Retail as Share of All Firms by Borough | Retail as Share of Borough Employment | Retail Loans Approved as Share of All Loans Approved |

Jobs Reported by PPP Retail Borrowers as Share of Jobs |

|

|---|---|---|---|---|---|---|---|

| Bronx | 3,757 | 30,786 | 20.6 | 16.9 | 22.7 | 11.3 | |

| Brooklyn | 9,623 | 73,158 | 15.1 | 15.3 | 15.6 | 10.0 | |

| Manhattan | 10,498 | 133,912 | 8.3 | 8.8 | 10.1 | 7.2 | |

| Queens | 7,297 | 59,342 | 13.8 | 14.3 | 14.4 | 9.8 | |

| Staten Island | 1,314 | 16,079 | 13.5 | 18.3 | 12.4 | 8.1 | |

| NYC | 32,488 | 313,277 | 12.0 | 11.7 | 13.3 | 8.6 | |

Note: All firms here have fewer than 500 employees.

Sources: U.S. Small Business Administration; NYS Department of Labor; OSC analysis

Many retailers reportedly had difficulty paying rents even before the pandemic. While retailers have been trying to creatively adjust to the changing business landscape as well as the pandemic, some have not been successful. The commercial real estate firm CBRE’s most recent quarterly retail report noted a new high of 254 available spaces in Manhattan’s 16 major retail corridors.9 Average asking rents in those corridors dropped under $700 per square foot, a level last seen in 2011. While the retail space within these corridors is also filled by other service providers (such as hair salons) and dining establishments, the report suggests that retailers, among others, are facing difficulty paying their rents given the decline of in-store revenues.

Federal Programs

Data from the U.S. Census Bureau’s Small Business Pulse Survey indicate that New York State’s retail firms have primarily relied on federal assistance for support to ease the effects of the pandemic.10 Retail firms sought assistance mainly from the Paycheck Protection Program (PPP), Economic Injury Disaster Loans (EIDLs) and the Small Business Administration’s Loan Forgiveness programs, while nonretail businesses sought relief from these as well as other federal programs and commercial banks.

EIDLs are nonforgivable, low-interest loans that provide working capital to small businesses suffering substantial economic injury due to the pandemic. Until June 11, 2020, these included a grant component in the form of a cash advance. EIDLs approved for New York State firms increased from 85,000 totaling $324 million at the beginning of April to 300,000 totaling $17.4 billion as of October 18, 2020. Pulse Survey data shows that a higher proportion of statewide retail businesses relied on EIDLs than those in any other small business sector.

The PPP provided forgivable loans to assist small businesses in retaining employees during the pandemic. PPP loans approved for the City’s retail sector rose sharply to a peak at the end of April, when the program was originally set to expire. After the program was extended and access made easier, especially for small firms, approximately 69 loans were approved each week from May 4 to August 8, 2020, when the program ended.

The share of loans approved for the retail sector represented 13 percent of all PPP loans approved in the City, which was higher than the sector’s share of all businesses (see Figure 8). More than 22 percent of total PPP recipient firms in the Bronx were in the retail sector. Conversely, retail’s share of all jobs reported for retention by PPP borrowers was lower than the sector’s share of employment citywide. PPP recipient firms in the retail sector were slightly larger than the average size of firms across all the City’s small businesses, with 11 employees compared to 10.

More than half (52 percent) of the City’s retail firms were approved for PPP loans. The number of retail jobs reported by these firms accounted for 38 percent of all retail sector jobs. Loans to food and beverage stores, health and personal care stores, and clothing and clothing accessories stores accounted for 57 percent of all retail sector loans and 62 percent of all retail sector jobs reported.

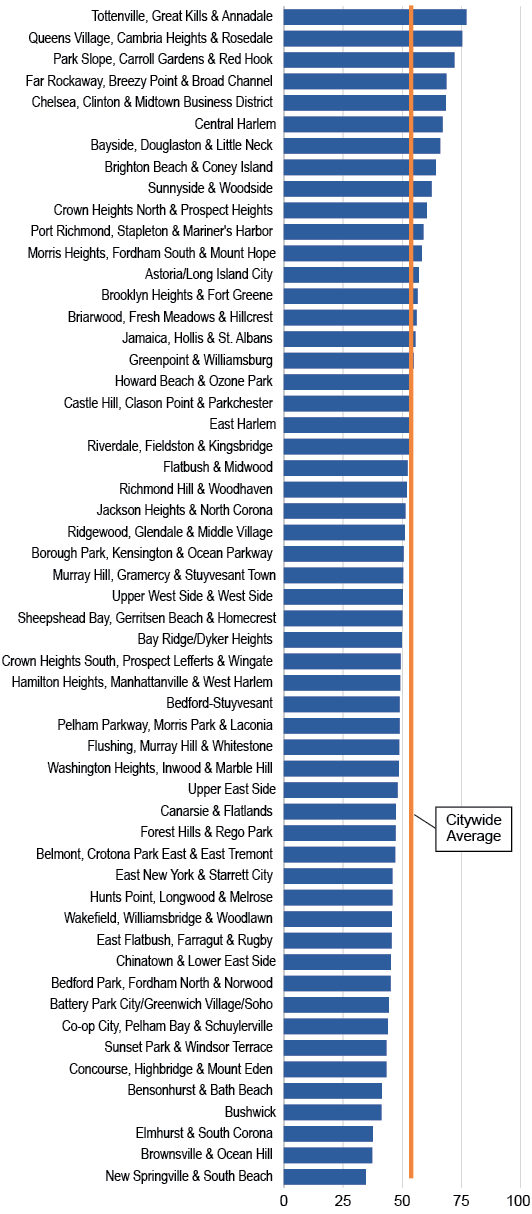

The extent to which retail establishments relied on PPP loans varied across the City’s neighborhoods (see Figure 9). Among the top 10 neighborhoods with the highest numbers of loans approved for retail, five were in Manhattan, four were in Brooklyn and one was in Queens. Manhattan neighborhood retailers accounted for just over half of all loans approved for clothing and clothing accessories stores, and sporting goods, hobby, music and book stores. Brooklyn firms accounted for nearly half of all loans approved for nonstore retailers.

FIGURE 9 - PPP Loans to Retail Firms as Share of Retail Firms with Fewer than 500 Employees

Sources: U.S. Small Business Administration; U.S. Census Bureau County Business Patterns, 2018; OSC analysis

Retail Sector: Looking Ahead

Retail is an important part of the fabric of New York City, and a true return to normal cannot be achieved without a robust and diverse retail sector. The ongoing effect of the pandemic on retailers in New York City has intensified previously identified trends toward online shopping and away from purchases of certain goods, such as clothing and sporting goods, from brick-and-mortar retailers. At the same time, basic consumer items such as groceries and medical items have received increased demand that is likely to stabilize over time.

The cumulative effect of these changes and what they mean for retail in the long term are still to be determined, but high-profile store closures indicate that certain subsectors may take longer to recover, while online shopping trends coupled with increased consumer preferences for contactless delivery may continue. Rising COVID-19 cases and hospitalizations entering the winter months is likely to extend industry uncertainty and would require more significant policy action to counter a renewal of slowed economic activity.

The uneven recovery in retail also muddies the policy landscape, and a more granular understanding of the issues facing different subsectors may be necessary in order to craft effective responses. Nevertheless, advocates agree that federal funding will play an important role for businesses and governments in mitigating the abrupt changes to regular individual consumer behavior. Industry participants also agree that some form of assistance is needed to manage the cost of rent in New York City, and the implications for tenants and landlords, while foot traffic and associated revenues are down.

Federal funding can support economic activity by extending expanded unemployment benefits and direct support to businesses that are fighting to remain open, such as the Paycheck Protection Program. Extensions of these or other similar programs can help to pay for labor and other expenses while encouraging spending, aiding retailer revenues and increasing taxable sales. Distributing more direct federal funds to state and local governments would also provide resources for creative programs at the local level, where additional support may otherwise be difficult given the widespread difficulties in balancing budgets at this time. Other jurisdictions have incentivized pop-up spaces, provided training on e-commerce, and created “microgrant” programs. The City and local community organizations have experience in connecting retailers to similar programs funded in the past. The Open Storefronts program provides one example of a shift in City policy based on dialogue with local store owners, and offers some support for retailers during the holiday season. Retailers recently suggested limited participation in the program so far could be increased by extending the program's expiration date. The City may take this recommendation under review.

In addition, the State and City governments have been called upon by business owners, landlords, and some legislators to provide resources to enable rent relief. Brick-and-mortar retailers, who have expressed concerns over the cost of rent in recent years, are now experiencing more acute need from the lack of revenues that used to come from their physical stores. An inability to pay rent will fall heavily on landlords, who argue they are unable to manage this burden alone. The City also has experience in administering commercial revitalization programs that leverage tax incentives to encourage small business activity. Any such programs would need to be weighed against their budgetary impacts and could be facilitated if funds from the federal government are forthcoming.

New York City is known for the diverse shopping experiences it provides, and the retail sector’s role in the overall appeal of the City is undeniable. In order for the City to fully serve its residents and regain its identity as a favored destination for visitors, a thriving retail sector must return.

1 The proposed legislation defines small businesses as those with no more than 25 employees.

2 Businesses providing services (such as hair salons) can also participate, but the services must be conducted inside the establishments, although products may be sold outdoors.

3 Unless otherwise indicated, data on employment and wages by place of work is from the New York State Department of Labor’s Quarterly Census of Employment and Wages (QCEW), and national data is from the U.S. Bureau of Labor Statistics. Updated U.S. 2019 data released with Q2 2020 was unavailable.

4 Neighborhoods in this report refer to the 55 U.S. Census-defined Public Use Microdata Areas (PUMAs) for New York City. For 2019 job and firm data, the neighborhoods match the geographic PUMA boundaries. Where data is reported by ZIP Code, allocation is made to neighborhoods using a crosswalk between ZIP Codes and PUMAs. This applies to PPP loans and County Business Patterns reports. For comparability purposes with PPP data, firm data was drawn from the 2018 County Business Patterns report, which is the most recent available.

5 All data on retail workers by place of residence are from the U.S. Census Bureau American Community Survey, 2019 1-year estimates, unless otherwise noted.

6 For a more detailed discussion of the slowdown in retail employment prior to the pandemic, see the “Retail Sector Profile” section earlier in this report.

7 A U.S. Supreme Court ruling in 2018 allowed states and localities to tax sales made to residents by out-of-state retailers that did not have a physical presence in the state. New York State sent notice of this rule to retailers in early 2019. In addition, a New York State tax law change that was implemented in June 2019 (the internet marketplace law) required some vendors to include an up-front sales tax charge on all online transactions to New York State residents.

8 Most food and beverages are not taxed in New York City, and therefore sales of these items are not included in the food and beverage subsector’s taxable sales. Candy, alcoholic beverages, soft drinks, prepared meals, and food and beverages sold for on-site consumption are taxable.

9 CBRE, Marketview: Manhattan Retail, Q3 2020.

10 According to the U.S. Census Bureau, the survey measures the effect of changing business conditions during the coronavirus pandemic.

APPENDIX A - New York City Retail Work Force by Neighborhood of Residence & Retail Businesses by Neighborhood of Location, 2019

| Neighborhood | Retail Workers | Share of Work Force | Share of Neighborhood Retail Workers | Retail Firms | |||||

| Immigrant | Hispanic or Latino | Asian | White | Black or African American |

Number | Share of All Firms | |||

| Jamaica/Hollis/St. Albans | 7,895 | 6.9 | 60 | 14.8 | 3.4 | 39.9 | 31.1 | 659 | 20.1 |

| Elmhurst/S. Corona | 7,603 | 9.1 | 68.3 | 50.2 | 0.8 | 4 | 43.1 | 412 | 18.9 |

| Belmont/Crotona Park East/East Tremont | 7,450 | 10.8 | 49.2 | 40.9 | 7.3 | 45 | 6.9 | 430 | 22.1 |

| Flushing/Murray Hill/Whitestone | 7,317 | 6.5 | 65.1 | 9.4 | 19.4 | 0 | 70.4 | 1,162 | 12.5 |

| Washington Heights/Inwood/Marble Hill | 6,594 | 5.9 | 49.5 | 71.1 | 9.8 | 13.9 | 3.3 | 610 | 19.1 |

| Castle Hill/Clason Point/Parkchester | 6,575 | 8.8 | 21 | 58.9 | 0.7 | 28.6 | 11 | 427 | 24.6 |

| Chinatown/Lower East Side | 5,873 | 7.1 | 32.9 | 17.2 | 25.4 | 26.3 | 24.7 | 862 | 13.9 |

| Queens Village/Cambria Heights/Rosedale | 5,708 | 5.9 | 47.8 | 22.8 | 12.4 | 40.7 | 21.7 | 332 | 11.9 |

| Bensonhurst/Bath Beach | 5,677 | 6.3 | 65.3 | 20.4 | 34.6 | 0 | 39 | 708 | 16.4 |

| Chelsea/Clinton/Midtown Business District | 5,474 | 4.9 | 18.6 | 26.9 | 60.2 | 0.4 | 10 | 3,301 | 7.3 |

| Astoria/Long Island City | 5,369 | 5.4 | 34.8 | 31.8 | 42.2 | 3.8 | 17.6 | 664 | 12 |

| Jackson Heights/North Corona | 5,322 | 6 | 74.4 | 68.7 | 12.5 | 3.9 | 14.9 | 685 | 20.7 |

| Canarsie/Flatlands | 5,293 | 5.4 | 48.6 | 14.8 | 22.3 | 47.9 | 11.7 | 519 | 16.9 |

| Bushwick | 4,915 | 6.8 | 32.9 | 40 | 20.8 | 27 | 9.1 | 427 | 18.4 |

| East New York/Starrett City | 4,749 | 6.7 | 47.1 | 37.5 | 0.6 | 54.5 | 6.2 | 452 | 25 |

| Tottenville/Great Kills/Annadale | 4,255 | 5.4 | 23.2 | 13.6 | 73.9 | 0 | 12.5 | 316 | 10.7 |

| Pelham Parkway/Morris Park/Laconia | 4,128 | 7 | 42.3 | 48.5 | 19.2 | 5.6 | 14 | 369 | 17.3 |

| Flatbush/Midwood | 4,091 | 5.7 | 59.2 | 6.3 | 35.6 | 40.9 | 11.1 | 521 | 15.8 |

| New Springville/South Beach | 4,060 | 6.3 | 60.8 | 7.1 | 60.8 | 0 | 30.1 | 510 | 14.8 |

| Port Richmond/Stapleton/Mariner's Harbor | 3,971 | 4.6 | 24.7 | 38.9 | 25.8 | 15.8 | 6.6 | 474 | 14.4 |

| Wakefield/Williamsbridge/Woodlawn | 3,917 | 5.9 | 52.4 | 23.5 | 2.3 | 68.1 | 0 | 265 | 17.5 |

| Sunset Park/Windsor Terrace | 3,885 | 6 | 68.8 | 31.6 | 2 | 4.7 | 58.8 | 816 | 17.7 |

| Bedford-Stuyvesant | 3,850 | 5.3 | 9.4 | 29.9 | 24.5 | 42.9 | 2.6 | 375 | 17.7 |

| Concourse/Highbridge/Mount Eden | 3,757 | 6.4 | 48 | 55 | 0 | 40.4 | 4.6 | 403 | 24.7 |

| Hunts Point/Longwood/Melrose | 3,670 | 6.8 | 39.4 | 79.1 | 0 | 20.9 | 0 | 603 | 20.5 |

| Brownsville/Ocean Hill | 3,589 | 7.3 | 29.6 | 34.8 | 6 | 56.6 | 0 | 330 | 28.5 |

| Sheepshead Bay/Gerritsen Bch./Homecrest | 3,582 | 5.4 | 63.1 | 6.8 | 49.4 | 0 | 27.7 | 713 | 14.2 |

| Briarwood/Fresh Meadows/Hillcrest | 3,551 | 4.5 | 58.4 | 4.9 | 14.4 | 12.3 | 63.4 | 356 | 12.9 |

| East Flatbush/Farragut/Rugby | 3,515 | 5.3 | 19.1 | 10.3 | 0.9 | 88.8 | 0 | 371 | 24.5 |

| Richmond Hill/Woodhaven | 3,398 | 4.7 | 55.7 | 39.9 | 7.7 | 2.2 | 35.7 | 400 | 14.9 |

| Greenpoint/Williamsburg | 3,385 | 3.9 | 20.3 | 16.7 | 76.4 | 0 | 6.9 | 973 | 14 |

| Bay Ridge/Dyker Heights | 3,384 | 5.7 | 63.9 | 44 | 26.8 | 1.5 | 25 | 445 | 13.8 |

| Ridgewood/Glendale/Middle Village | 3,349 | 4 | 28.2 | 23 | 45.7 | 12.5 | 13.2 | 601 | 15.3 |

| Hamilton Heights/Manhattanville/W. Harlem | 3,339 | 4.4 | 30.3 | 44.2 | 30.5 | 24 | 0 | 260 | 11.8 |

| Bedford Park/Fordham N./Norwood | 3,337 | 4.8 | 51.6 | 51 | 17.6 | 16.6 | 14.8 | 370 | 23.8 |

| Central Harlem | 3,094 | 4.4 | 12.3 | 31.1 | 14.4 | 54.5 | 0 | 297 | 13.8 |

| Crown Heights S./Prospect Lefferts/Wingate | 2,943 | 5.2 | 34 | 13.7 | 9.3 | 73.9 | 3 | 293 | 19.3 |

| Murray Hill/Gramercy/Stuyvesant Town | 2,915 | 2.9 | 14.8 | 0 | 81.4 | 0.3 | 18.2 | 828 | 4.7 |

| Co-op City/Pelham Bay/Schuylerville | 2,838 | 5.4 | 44.8 | 21.7 | 18.4 | 56.6 | 3.3 | 287 | 18.4 |

| Bayside/Douglaston/Little Neck | 2,824 | 4.9 | 43 | 10.8 | 46 | 0 | 40.8 | 317 | 9.7 |

| Far Rockaway/Breezy Pt./Broad Channel | 2,772 | 5.7 | 38.9 | 26.2 | 22.5 | 44.6 | 2.6 | 188 | 14.9 |

| Brooklyn Heights/Fort Greene | 2,680 | 3.5 | 15.2 | 5.2 | 66 | 24.6 | 4.3 | 653 | 9.7 |

| Howard Beach/Ozone Park | 2,616 | 4.2 | 55.1 | 32.2 | 0 | 13.2 | 50.7 | 361 | 18.6 |

| Morris Heights/Fordham S./Mount Hope | 2,547 | 4.7 | 58 | 73.7 | 0 | 20 | 0 | 367 | 26.7 |

| Brighton Beach/Coney Island | 2,544 | 5.8 | 72.4 | 23.5 | 37.6 | 0 | 35.5 | 391 | 15.4 |

| Sunnyside/Woodside | 2,471 | 3.2 | 68.9 | 33.4 | 8.7 | 0 | 55.6 | 585 | 11 |

| Crown Heights N./Prospect Heights | 2,459 | 3.5 | 9.4 | 16.2 | 30.7 | 49.3 | 0 | 320 | 13.4 |

| East Harlem | 2,400 | 5.1 | 37 | 29.7 | 10.6 | 41 | 18.8 | 354 | 18.2 |

| Borough Park/Kensington/Ocean Pkwy. | 2,219 | 4.1 | 30.4 | 9.2 | 67.9 | 0 | 22.8 | 877 | 15.5 |

| Forest Hills/Rego Park | 2,159 | 3.9 | 60.6 | 7.9 | 59.9 | 0 | 32.2 | 398 | 11.6 |

| Battery Park City/Greenwich Village/Soho | 2,012 | 1.9 | 41.1 | 0 | 71.4 | 0 | 28.6 | 2,072 | 8.9 |

| Upper West Side/West Side | 1,982 | 1.9 | 10.3 | 35.7 | 60.8 | 3.5 | 0 | 529 | 6.1 |

| Upper East Side | 1,802 | 1.5 | 5.5 | 14.9 | 85.1 | 0 | 0 | 1,122 | 8.5 |

| Riverdale/Fieldston/Kingsbridge | 1,796 | 4 | 49 | 76.8 | 12.5 | 5 | 0 | 199 | 10.9 |

| Park Slope/Carroll Gardens/Red Hook | 1,724 | 2.5 | 15.7 | 20.4 | 59 | 0 | 20.6 | 452 | 9.1 |

| NYC | 214,624 | 5.2 | 43.7 | 30.7 | 24.6 | 22.2 | 19.2 | 32,600 | 12.0 |

Note: Citywide figures for firms reflect latest 2019 QCEW data. Neighborhood-level data may not add up due to rounding and timing of microdata release.

Sources: U.S. Census Bureau, American Community Survey, 2019 1-yr estimates; NYS Department of Labor, QCEW 2019; OSC analysis