State Fiscal Year 2022-23 Enacted Budget Analysis

May 2022

The New York State Budget for State Fiscal Year (SFY) 2022-23 was adopted on April 9, 2022. The Executive and the Assembly Ways and Means Committee have indicated that All Funds spending will total $220.5 billion in SFY 2022-23. The Budget was adopted following two years of extraordinary volatility in State finances that began with the unprecedented economic disruptions caused by the COVID-19 pandemic and the prospect of steep revenue shortfalls. In response, the State received historic federal financial assistance and enacted tax increases. Economic performance also surpassed expectations, generating unanticipated revenues. These factors have allowed for a steep increase in spending, both for temporary investments for pandemic-related needs and expanded or new commitments to existing programs.

The Enacted Budget Financial Plan, required to be published no later than May 19, will provide detailed estimates from the Division of the Budget (DOB) of SFY 2022-23 revenues and expenditures by source and purpose, and offer critical insight into the short- and long-term implications of the recently adopted budget. This report provides a preliminary review of the Enacted Budget based upon actual results from the three most recently completed State fiscal years, as well as estimates for SFY 2022-23 based upon enacted appropriations and information presently available from DOB and the New York State Assembly. The Office of the State Comptroller will complete a detailed analysis of the Enacted Budget Financial Plan report and provide a comprehensive assessment in the weeks ahead.

Spending Overview

As shown in Figure 1, reported All Funds spending in SFY 2022-23 is projected to be 5.3 percent higher than SFY 2021-22 and nearly 27.5 percent higher than SFY 2019-20, the last full fiscal year before the onset of the COVID-19 pandemic, an increase of $47.5 billion dollars over this time period.

FIGURE 1: All Funds Revenue and Spending, SFY 2019‑20 to SFY 2022‑23

(dollars in millions)

| SFY 2019-20 Actual | SFY 2020-21 Actual | SFY 2021-22 Actual (Unaudited) | SFY 2022-23 Estimate | SFY 2019-20 to SFY 2022-23 Change | |||||

|---|---|---|---|---|---|---|---|---|---|

| Amount | Amount | Percent Change | Amount | Percent Change | Amount | Percent Change | Amount | Percent Change | |

| Personal Income Tax | $53,659 | $54,967 | 2.4% | $70,737 | 28.7% | $48,551 | -31.4% | -$5,108 | -9.5% |

| Consumption/Use Taxes | $18,022 | $16,117 | -10.6% | $19,621 | 21.7% | $19,600 | -0.1% | $1,578 | 8.8% |

| Business Taxes | $8,996 | $8,792 | -2.3% | $27,725 | 215.3% | $27,870 | 0.5% | $18,874 | 209.8% |

| Other Taxes | $2,212 | $2,499 | 13.0% | $3,053 | 22.1% | $2,577 | -15.6% | $365 | 16.5% |

| Total All Funds Taxes | $82,889 | $82,376 | -0.6% | $121,136 | 47.1% | $98,598 | -18.6% | $15,709 | 19.0% |

| Miscellaneous Receipts | $29,466 | $30,772 | 4.4% | $27,932 | -9.2% | $27,514 | -1.5% | -$1,952 | -6.6% |

| Federal Receipts | $65,080 | $78,152 | 20.1% | $95,306 | 21.9% | $84,444 | -11.4% | $19,364 | 29.8% |

| Total All Funds Revenue | $177,435 | $191,300 | 7.8% | $244,375 | 27.7% | $210,556 | -13.8% | $33,121 | 18.7% |

| Total All Funds Spending | $172,980 | $186,587 | 7.9% | $209,339 | 12.2% | $220,472 | 5.3% | $47,492 | 27.5% |

Note: SFY 2022-23 estimates are DOB projections included in the FY 2023 Executive Budget Financial Plan Updated for 30-Day Amendments adjusted for provisions included in the Enacted Budget. All Funds spending projection in SFY 2022-23 is from the New York State Assembly.

All Funds spending increased 21 percent between SFY 2019-20 and SFY 2021-22. Spending growth between SFY 2019-20 and SFY 2021-22 would have been lower absent a number of financial management actions, notably $7.6 billion in debt service prepayments made at the end of March. The prepayments increased spending in SFY 2021-22 and reduced necessary spending in SFY 2022-23 and later years. Without these debt management actions, growth would have been 16.6 percent.

Education and Medicaid are the two largest components of the State Budget, and have also typically been the largest drivers of spending growth. Education spending increased more than 10 percent and Medicaid increased 13.6 percent between SFY 2019-20 and SFY 2021-22. According to the initial 2022-23 State Aid Projections (“School Aid Runs”) published by the State Education Department, school aid is expected to increase from $28.8 billion in school year (SY) 2021-22 to $30.9 billion in SY 2022-23, an increase of $2.1 billion, or 7.2 percent. Reflecting the second year of a three-year plan to fully fund the Foundation Aid formula, Foundation Aid is projected to total $21.3 billion in SY 2022-23, an increase of $1.5 billion or 7.7 percent. Another notable increase is for funding for universal pre-kindergarten (UPK) services, which is expected to grow by 11.3 percent, or $106.6 million, to more than $1 billion.

Allowable Department of Health (DOH) State Funds Medicaid spending under the “global cap” of $25.9 billion in SFY 2022-23 was unchanged from Executive to Enacted Budget appropriation legislation, but is expected to rise by $262 million to $27.7 billion for SFY 2023-24.1 The increase reflects, in part, additions for safety net hospitals ($900 million), long-term care services, including home care minimum wage increases ($565 million), pharmacy services ($90 million) and transportation services ($8 million), offset by reductions for managed care plans ($951 million), mental hygiene programs shifted from the General Fund to the Medicaid global cap ($332.6 million), and for non-institutional services ($168 million).

Other notable spending increases in SFY 2022-23 are intended to address impacts of the COVID-19 pandemic on New Yorkers and on the health care system, including front-line workers. The Enacted Budget includes $2 billion in one-time pandemic-related assistance for multiple initiatives, including an additional $800 million for the Emergency Rental Assistance Program (ERAP) that provides aid to eligible households facing housing instability or homelessness and with earnings at or below 80 percent of area median income for rental payments or rental and utility arrears accumulated since the start of the pandemic. The additional appropriation brings the State’s total funding for ERAP to more than $1 billion. (See the Office of the State Comptroller’s COVID-19 Relief Program Tracker for more details on this program.)

An additional $250 million was added specifically for utility bill arrears, $125 million for homeowner and landlord assistance, and $15 million for other one-time programs. Finally, $800 million in funding was added for hospitals continuing to experience financial distress emanating from care provided during the pandemic.

The Enacted Budget also plans for $1.27 billion in State funds to provide health care and mental hygiene worker bonuses in SFY 2022-23. Employees are eligible for bonus payments of $500, $1,000 and $1,500 depending on the average number of hours continuously worked per week during 6-month “vesting” periods from October 2021 through March 2024, with total bonus payments not exceeding $3,000 per employee across all employers. The funding is allocated as $1.13 billion in local assistance for certain workers receiving an annualized base salary of $125,000 or less; and $136 million in State operations expenses, for workers in State-operated facilities, institutional or direct-care settings operated by the State, or State University of New York (SUNY) public hospitals.

The Enacted Budget also includes new spending for child care, both to help stabilize providers and to expand subsidies to families. Through March 2022, $868.2 million in stabilization grants were made to providers; the Enacted Budget adds $343 million for another round of grants, with requirements that at least 75 percent be used for workforce initiatives such as wage increases, bonuses, tuition reimbursement, and contributions to staff retirement plans and health insurance costs.

Starting August 1, 2022, eligibility for child care subsidies will expand from 200 percent to 300 percent of the federal poverty level. For families receiving subsidies, co-payments will be limited to 10 percent of family income above the federal poverty level. Local social service districts will be required to pay for up to 24 absences per child per provider per year, and the subsidy market rate (i.e., the maximum rate at which the State makes subsidy payments) will grow from the 69th to the 80th percentile of amounts that families pay for child care, expanding opportunities for access. Under these provisions, child care subsidies would rise to $1.32 billion in SFY 2022-23 and grow in subsequent years. The Enacted Budget also includes two tax measures to incentivize creation of additional child care slots in New York City.2

Revenue Overview

Based upon the most recent Financial Plan released in conjunction with 30-Day Amendments to the Executive Budget, as well as DOB estimates for revenue actions included in the Enacted Budget, All Funds revenues for SFY 2022-23 are projected to total $210.6 billion, 13.8 percent lower than SFY 2021-22 but 18.7 percent higher than SFY 2019-20. Collections during this period have been remarkably volatile due to rapidly changing economic conditions during the early days of the pandemic, an unprecedented influx of temporary federal aid, and changes in tax policies.

While taxes were initially projected to decline steeply in SFY 2020-21, the decline proved to be more moderate than expected. Consumption taxes, especially the sales and use tax, were most adversely impacted in SFY 2020-21, decreasing by 10.6 percent. Similarly, total business taxes declined by $203.4 million, or 2.3 percent, reflecting the impact of the pandemic-related shutdown and restrictions on certain business sectors.

Personal income tax (PIT) collections, in contrast, continued to grow, rising by $1.3 billion or 2.4 percent, in SFY 2020-21. The financial markets hit record levels in 2020, and Finance and Insurance sector bonuses increased by 12.9 percent. In addition, since unemployment benefits are taxable income under the PIT, the enhanced payments provided through the federal pandemic unemployment programs propped up collections, as well.

In addition to payments made directly to individuals, temporary federal assistance was provided to the State to deal with the impacts of the pandemic and offset revenue losses, with receipts growing by more than 20 percent in SFYs 2020-21 and 2021-22 to reach more than $95.3 billion in SFY 2021-22. The State received $12.7 billion in State Fiscal Recovery Funding from the American Rescue Plan alone, with $4.5 billion of that funding deposited to the General Fund at the end of SFY 2021-22. Federal receipts will decline this year and in subsequent years as relief funds are depleted.

In addition to extraordinary federal aid, tax collections rebounded strongly in SFY 2021-22, as financial markets remained strong, financial sector bonuses grew, and employment recovery continued. In addition, tax rates were increased on businesses and high-income taxpayers beginning in the 2021 tax year. The PIT rate increases on high-income taxpayers, which will sunset on December 31, 2027, were estimated to generate $2.7 billion in SFY 2021-22. The increased corporate franchise tax rates were estimated to generate $750 million in SFY 2021-22 and will sunset on December 31, 2023.

Extraordinarily high business tax collections in SFY 2021-22 also reflect the impact of the pass-through entity tax (PTET), which allows certain businesses to make payments that are later credited via the personal income tax. Due largely to the PTET credit, SFY 2022-23 PIT receipts are projected to decline by $22.2 billion or 31.4 percent.3

SFY 2022-23 All Funds revenues are projected to decrease by $33.8 billion, or 13.8 percent, due to a variety of factors. Economic growth is forecasted to slow after the surge resulting from the lifting of the pandemic shutdowns and restrictions; PIT collections will be affected by the offsetting impact from the PTET; federal relief is spent down; and several provisions included in the Enacted Budget will reduce tax collections by $3.5 billion, including:

- $2.2 billion to provide one-time rebates to property taxpayers throughout the State with income less than $250,000.

- $585 million for the suspension of the State excise and sales taxes on motor fuel from June through December 2022, resulting in a reduction of 16 cents in the pump price of gasoline per gallon.

- $162 million for the acceleration of the middle-class personal income tax rate reductions from 2025 to 2023.

Reserve Funds

At the close of SFY 2021-22, the State added $843 million to its statutory rainy day reserve funds, bringing the total balance up to $3.3 billion, an amount equal to 3.7 percent of General Fund spending. The Enacted Budget includes authorization to increase the maximum level of deposits to statutory rainy day fund reserves from 5 to 15 percent of General Fund spending. It also increased the maximum allowable annual deposits from 0.75 percent to 3 percent of General Fund spending. Although the Governor indicates that $15.5 billion of new resources, including deposits to the rainy day reserves and informal reserves, will be set aside through SFY 2024-25, the apportionment between statutory and informal reserves is not yet publicly available.4

FIGURE 2: State Reserve Funds, SFY 2020-21 to SFY 2021-22

(dollars in millions)

| SFY 2020-21 Actual | SFY 2021-22 Enacted Projection | SFY 2021-22 February 2022 Projection | SFY 2021-22 Actual (Unaudited) | Change, SFY 2020-21 Actual to SFY 2021-22 Actual |

||

|---|---|---|---|---|---|---|

| Closing General Fund Balance | $9,161 | $7,354 | $30,513 | $33,053 | $23,892 | |

| Statutory Rainy Day Funds | $2,476 | $3,301 | $3,351 | $3,319 | $843 | |

| Tax Stabilization Reserve Fund | $1,258 | $1,433 | $1,433 | $1,435 | $177 | |

| Rainy Day Reserve Fund | $1,218 | $1,868 | $1,918 | $1,884 | $666 | |

| Informal Reserves | ||||||

| Economic Uncertainties1 | $1,490 | $1,490 | $5,598 | N/A | N/A | |

| Total "Principal Reserves"2 | $3,966 | $4,791 | $8,949 | N/A | N/A | |

| Other General Fund Uses3 | $5,195 | $2,563 | $21,564 | $29,734 | $24,539 | |

Sources: Division of the Budget; Office of the State Comptroller

1 Fund for Economic Uncertainties is not a statutorily created fund like Tax Stabilization and Rainy Day Reserve Funds. The resources set aside for Economic Uncertainties can be used for any appropriated purpose at any time.

2 Principal Reserves as defined by the Division of the Budget.

3 Other General Fund Uses include funds set aside for PTET and PIT credits, future labor costs and State operations costs, costs associated with debt management, appropriated monetary settlements that have not been disbursed or transferred to another fund, and funding set aside for economic uncertainties. In addition, it includes the Contingency Reserve Fund and the Community Projects Fund, two statutory reserves.

Capital Projects and Debt Implications

The Enacted Budget includes revisions to the Clean Water, Clean Air, and Green Jobs Environmental Bond Act that will be presented to the voters for consideration in November 2022. The Bond Act is intended to support investments to protect communities and their residents from the hazards of extreme weather; mitigate greenhouse gas and other air pollutant emissions; improve drinking and surface water quality; and advance State goals for protecting vital habitats and promoting outdoor recreation. Funding allocations for the $4.2 billion Environmental Bond Act were changed from the Executive proposal, and now total:

- $1.1 billion for aquatic restoration and flood risk reduction;

- $650 million for open space conservation, with farmland protection funded at $150 million;

- $1.5 billion for climate change mitigation, with green buildings funded at $400 million and new funding allocations for: zero emission transportation, $500 million; climate adaptation and mitigation, $100 million; and reduction of impacts of water and air pollution on disadvantaged communities, $200 million;

- $650 million for water quality improvement and resilient infrastructure, with municipal stormwater grants increased to $250 million; and

- $300 million for projects to preserve, enhance and restore New York’s natural resources and reduce the impacts of climate change.

Voters will have the opportunity to weigh in directly on the Bond Act, an important accountability mechanism for keeping the State’s debt burden affordable, and the State’s capital and debt projections have taken voter approval into account. In contrast, the Enacted Budget adds $21.7 billion in debt authorizations above last year’s level, which will be undertaken as “backdoor borrowing” by public authorities on behalf of the State. These new authorizations may further reduce available State debt capacity under the Debt Reform Act limitations, which was projected to be $673 million by SFY 2026-27. This limited capacity is despite the exclusion of $2.35 billion in new debt anticipated to be incurred for the Gateway Program and after an estimated $19 billion in debt issuances excluded from the cap over the last two years.

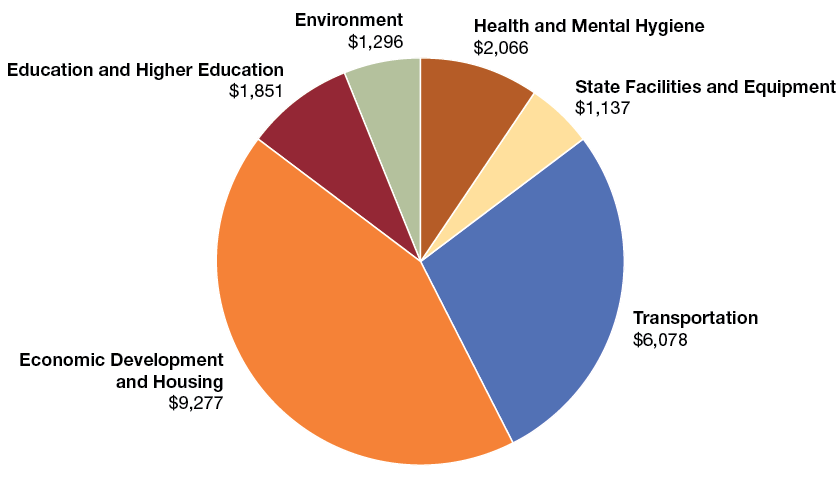

As shown in Figure 3, more than 70 percent of the $21.7 billion increase is for housing, economic development, and transportation, including $2.35 billion for the Hudson Tunnel Project, part of the Gateway Program to improve rail infrastructure between New York and New Jersey.

FIGURE 3: New Debt Authorizations by Functional Area, SFY 2021-22 to SFY 2022-23

(dollars in millions)

Sources: Division of the Budget; Office of the State Comptroller

Notable debt authorization increases from the Executive Budget proposal include: $1 billion for economic development purposes, including the State’s commitment for the new Buffalo Bills stadium; $631 million for housing programs; and $396 million for projects at the State and City Universities of New York.

FIGURE 4: Debt Authorization Increases by Purpose, SFY 2021-22 to SFY 2022-23

(dollars in millions)

| Program | Current Cap1 | SFY 2022-23 Enacted Cap | Change from Current Cap |

|---|---|---|---|

| Housing Capital Programs | $ 7,545.1 | $ 13,082.9 | $ 5,537.8 |

| Economic Development Initiatives | 11,279.2 | 14,968.4 | 3,689.2 |

| Gateway Program | – | 2,350.0 | 2,350.0 |

| Dedicated Highway & Bridge Trust | 18,150.0 | 19,776.9 | 1,626.9 |

| Health Care Initiatives | 3,053.0 | 4,653.0 | 1,600.0 |

| Transportation Initiatives | 8,840.0 | 10,147.9 | 1,307.9 |

| SUNY Educational Facilities | 15,555.9 | 16,611.6 | 1,055.7 |

| Environmental Infrastructure Projects | 7,130.0 | 8,171.1 | 1,041.1 |

| Consolidated Highway Improvement Program (CHIPS) | 12,260.5 | 13,053.9 | 793.4 |

| CUNY Educational Facilities | 9,661.0 | 10,254.7 | 593.7 |

| Mental Health Facilities | 10,476.8 | 10,942.8 | 466.1 |

| Prison Facilities | 9,139.6 | 9,502.7 | 363.1 |

| State Office Buildings and Other Facilities | 1,308.7 | 1,605.0 | 296.3 |

| Energy Efficiency Projects/NYPA Refunding | – | 200.0 | 200.0 |

| Information Technology | 974.3 | 1,152.6 | 178.3 |

| Statewide Equipment | 293.0 | 393.0 | 100.0 |

| Youth Facilities | 876.0 | 962.7 | 86.7 |

| Special Education and Other Educational Facilities | 236.0 | 301.7 | 65.7 |

| SUNY Upstate Community Colleges | 1,066.3 | 1,123.1 | 56.9 |

| Water Pollution Control (State Revolving Fund) | 1,030.0 | 1,085.0 | 55.0 |

| Division of State Police | 374.6 | 426.1 | 51.5 |

| Nonprofit Infrastructure Capital Investment Program | 120.0 | 170.0 | 50.0 |

| Higher Education Capital Matching Grants | 300.0 | 345.0 | 45.0 |

| Homeland Security and Training Facilities | 347.5 | 383.5 | 36.0 |

| Library Facilities | 299.0 | 333.0 | 34.0 |

| Division of Military & Naval Affairs | 172.0 | 197.0 | 25.0 |

| Food Laboratory | 40.7 | 40.8 | 0.1 |

| Total Public Authority Bond Caps with Changes | $ 120,529.1 | $ 142,234.4 | $ 21,705.3 |

| All Other Public Authority Bond Caps | 43,704.8 | 43,704.8 | – |

| Total Public Authority Bond Caps | $ 164,233.9 | $ 185,939.2 | $ 21,705.3 |

| General Obligation Bond Act Authorizations2 | 18,935.0 | 23,135.0 | 4,200.0 |

| Total State-Supported Bond Caps/Authorizations3 | $ 183,168.9 | $ 209,074.2 | $ 25,905.3 |

Sources: Division of the Budget; Office of the State Comptroller

Note: Totals may not add due to rounding.

1 The current cap reflects the amount previously authorized, some or all of which may already have been issued.

2 This table reflects General Obligation Bond Acts for which there is a remaining authorized but unissued amount and/or a remaining debt outstanding balance. The increase in the General Obligation Bond Act Authorizations reflects the modification of the Restore Mother Nature Bond Act authorization, enacted in SFY 2020-21. The Executive proposal increased the amount in the authorization from $3 billion to $4 billion and changed the name to the Clean Water, Clean Air and Green Jobs Environmental Bond Act. The Enacted Budget increased the authorization to $4.2 billion and accepted the proposed name change.

3 The Enacted Budget accepted temporary financing of up to $5 billion through PIT revenue anticipation notes ($3 billion) and line of credit facilities ($2 billion). These amounts are not subject to the limitations of the Debt Reform Act.

Several new discretionary lump-sum capital appropriations were added, with little detail regarding intended purposes, such as:

- $800 million for the New York State Regional Economic and Community Assistance Program to “foster regional workforce and commercial development, tourism and infrastructure improvement, community and urban revitalization, small business support, local community priority projects and other economic development;”

- $385 million for the Community Resiliency, Economic Sustainability and Technology Program to support “projects intended to improve the quality of life of the residents of the State of New York through investment in facilities which support arts, cultural, athletic, housing, child care, educational, parks and recreational, transportation, port development, economic development, workforce training, employment development, tourism, community redevelopment, climate change mitigation, resiliency, environmental sustainability, and other civic activities;”

- $350 million for the Long Island Investment Fund to support “manufacturing, agriculture, business parks, community anchor facilities, advanced technology, biotechnology and biomedical, and main street revitalization;” and

- $185 million for the Local Community Assistance Program to “support community development or redevelopment, revitalization, economic development, economic sustainability, arts and cultural development, housing, public security and safety and local infrastructure improvement or enhancement.”

Transparency, Accountability and Oversight

Transparency, accountability and independent oversight are keys to ensuring that public resources are protected from waste, fraud and abuse, and that the public has access to important information regarding government activities. While the Enacted Budget makes some improvements in this respect—for example, including statutory requirements for information published in the “database of deals” for economic development projects from 2018 on and requiring an analysis of all current economic development tax incentives—there are many provisions that weaken essential protections, leaving public resources more vulnerable to misuse, and potentially diminishing New Yorkers’ confidence in their State government.

Independent Oversight and Procurement Integrity Provisions

Under Section 112 of the State Finance Law (SFL), the Office of the State Comptroller conducts an independent review of many State agency contracts. Under Section 2879-a of the Public Authorities Law (PAL), the Comptroller also has the authority to review certain public authority contracts. This independent review protects taxpayers, agencies, not-for-profit organizations and other vendors by validating that a contract’s costs are reasonable, its terms are favorable to the State, and that all bidders are treated the same. Such an independent review serves as an important deterrent to waste, fraud and abuse, further ensures that the State is contracting with responsible vendors and increases transparency in State procurement.

Executive and Legislative actions over the past decade have eroded this contract approval authority by bypassing SFL Section 112, and PAL Section 2879-a. The Enacted Budget did not include any provisions to rectify these actions, and further diminished contract approval authority by including appropriations and other provisions that bypass these sections of law. In addition, many provisions also waive competitive bidding requirements for State contracts.

Provisions in the Enacted Budget notwithstanding SFL Section 112 and PAL Section 2879-a total at least $11 billion. However, it is important to note that there are several new provisions included in various Article VII bills that did not include appropriations, but which include language that bypasses these sections of law and could increase the impacted amount.

Examples where the Comptroller’s contract oversight and competitive bidding are eliminated include:

- A $6 billion appropriation for transfer by the Executive to certain funds to cover services and expenses related to the COVID-19 outbreak including but not limited to additional personnel, equipment and supplies, travel costs and training, as well as responding to the direct and indirect economic, financial, or social effects of COVID-19; and

- A $2 billion appropriation solely for transfer by the Executive to certain funds to meet “unanticipated emergencies” pursuant to purposes set forth in SFL Section 53.

The Enacted Budget also includes $1.6 billion through the Health Care Facility Transformation Program for capital project grants for eligible health care providers, most of which is exempted from the Comptroller’s contract pre-review oversight authority pursuant to SFL Section 112. Also, grants are authorized to be awarded pursuant to a process approved administratively, not the competitive bidding process required by law.

The Enacted Budget includes a provision to require DOH to procure an independent contractor without the Comptroller’s contract pre-review or SFL competitive bidding requirements, to review and make recommendations concerning the status of services offered by managed care organizations contracting with the State to manage services provided under the Medicaid program. This provision bypasses important oversight and accountability requirements for the selection of a contractor who will make recommendations on how potentially billions of dollars for Medicaid services will be awarded.

Executive Discretion to Manage and/or Reshape the Budget

Several components of the Enacted Budget fall short with respect to high standards of transparency, accountability and oversight, including language in several appropriations which provides significant flexibility to the Executive after enactment of the Budget regarding the use of billions of dollars of spending. This flexibility creates uncertainty as to how their use might affect important programs and services, State agencies, local governments, nonprofit organizations and individual New Yorkers who rely on State funding.

The Enacted Budget includes new federal and emergency appropriations totaling at least $18 billion that are unnecessarily opaque with respect to how the State would use these funds. In addition to the lack of transparency with respect to the intended use of these funds, these broad-scoped appropriations may leave the allocation of such funds almost entirely to Executive discretion.

Use of Lump-Sum and Other Broad-Scoped Appropriations

The Enacted Budget continues and expands the State’s use of lump-sum and other broad-scoped appropriations for yet-to-be-determined projects and purposes. In an effort to improve transparency and accountability in the State’s spending, the Budget Reform Act of 2007 prohibited the use of lump-sum appropriations by the Legislature, with more limited restrictions for the Executive.5 The statutory prohibition can, however, be circumvented in various ways. Examples of lump-sum or other broad-scoped appropriations in the Enacted Budget are outlined below.

- The Enacted Budget provides for the transfer of $1 billion from the General Fund to the Health Care Transformation Fund. Moneys in this Fund are authorized to be transferred to any other fund of the State, as authorized and directed by DOB, to support health care delivery. The provisions of the Fund allow the expenditure of State resources to support health care delivery, including capital investment, debt retirement or restructuring, housing and other social determinants of health, or transitional operating support to health care providers.

- The Enacted Budget includes new broad-scoped capital projects appropriations with undefined projects or criteria for their use. Examples include $800 million for the New York State Regional Economic and Community Assistance Program, $385 million for the Community Resiliency, Economic Sustainability and Technology Program, $350 million for the Long Island Investment Fund, and $185 million for the Local Community Assistance Program. While the projects and purposes these funds are intended to support may be worthwhile, using lump-sum appropriations results in less transparent mechanisms to distribute hundreds of millions of dollars, providing minimal disclosure of decision making regarding the allocation of funds, the intended recipients of such funding, specific expenditures and the potential benefits of such spending for New Yorkers. State dollars should be allocated in a fair, objective, and transparent manner, with information about actual expenditures made public in a timely and detailed manner.

- The Enacted Budget includes $2.2 billion in reappropriations for the State and Municipal Facilities Program (SAM). This bond-financed program was first enacted in SFY 2013-14, and subsequent budgets added additional appropriation and bonding authority. The allowed uses of such moneys include a broad range of economic development, education, environmental and other purposes. However, the Budget does not include specific language to provide for the distribution of these moneys among the various purposes or among the various entities authorized to receive funding, or even to outline the process by which such funds will be allocated.

Debt Accountability

The Enacted Budget includes a $2.35 billion State commitment to repay a federal transportation loan for the Gateway Program in a manner that allows this obligation to circumvent the State’s statutory debt caps. Since the Debt Reform Act only counts “bonds or notes,” this utilizes a loophole to incur debt outside of the State’s debt cap through the federal loan. This loan would otherwise meet all of the criteria of being State-supported debt by a) incurring debt (albeit in the form of a loan, rather than “bonds or notes”), b) contractually obligating the State to repay such debt through a service contract mechanism, subject to legislative appropriation, and c) being issued for a State capital purpose, New York’s $2.35 billion share of the total project costs.

In addition, the Enacted Budget again includes authorizations for up to $5 billion in short-term cash flow borrowings during SFY 2022-23, through $3 billion in PIT Notes and $2 billion in lines of credit. Given the State’s currently strong fiscal position, the authorizations for these more costly forms of borrowing otherwise serve only to circumvent the State’s Local Government Assistance Corporation reforms, which require the declaration of emergency or extraordinary factors needed before issuing lower-cost State Tax and Revenue Anticipation Notes (TRANs).

Special Revenue Fund Sweeps

The Enacted Budget includes the authorization for DOB to sweep up to $700 million in unspecified transfers from dedicated funds to the General Fund, the same amount as was authorized in SFY 2021-22. Since SFY 2007-08, budget language has authorized DOB to transfer or “sweep,” at its discretion, available, unencumbered resources from other State funds to the General Fund. More than $2.1 billion has been swept from special revenue funds to the General Fund using this authority. The unidentified programs which may be affected are generally programs that have dedicated revenue streams. Any use of such sweeps could undermine the purposes for which the funds were originally generated and dedicated.

Accounting Standards

Many appropriations throughout the Enacted Budget include language which authorizes spending “net of refunds” and other credits to the State, as well as language expressly directing the Comptroller to credit such refunds to the original appropriation and “reduce expenditures in the year which such credit is received regardless of the timing of the initial expenditure.” These provisions, which do not include any dollar limitation, have the potential to artificially reduce the appearance of true liabilities and reported receipts and disbursements of the State in a given fiscal year.

In addition, the Budget includes language, first enacted in SFY 2020-21, expressly directing the Office of the State Comptroller to credit the original appropriation and “reduce expenditures in the year in which such credit is received regardless of the timing of the initial expenditure.” These provisions, which do not include any dollar limitation, could result in actual spending beyond amounts set forth in the appropriation in a given fiscal year, and may further cloud the picture of true spending growth.

Conclusion

The SFY 2022-23 Enacted Budget was adopted following two years of extraordinary volatility in State finances. Significant increases in tax resources and federal aid have led to substantial growth in spending for relief programs, new initiatives, and expanded commitments to existing programs. While some of this spending will be temporary, much of it will be recurring; pending the release of the Financial Plan, it is unclear how projected spending growth will track with anticipated growth in State-sourced revenues.

While the State’s financial position currently appears strong, sustaining new recurring commitments over a longer time period may be difficult, as new economic risks emerge, federal funds are spent down, and temporary tax revenues sunset. Bolstering reserve funds is essential for ensuring services New Yorkers rely on can be preserved through economic challenges and fiscal uncertainties, and every opportunity should be taken to maximize deposits to the State’s statutory rainy day reserve funds.

The growth in capital projects spending and related debt service may also result in additional pressure on the Financial Plan, particularly in the event of an economic downturn that would reduce State revenues. Policymakers should seek to utilize pay-as-you-go financing, rather than debt, to the greatest extent possible.

The Office of the State Comptroller will provide an in-depth of analysis of operating spending, capital commitments and debt affordability after the Enacted Budget Financial Plan is released.

Endnotes

1 The Medicaid global cap was extended through SFY 2023-24, but calculation of the cap was changed to the 5-year rolling average of annual health care spending projections by the Centers for Medicare and Medicaid Services. Previously, the cap was calculated on a 10-year rolling average of medical inflation.

2 First, the Child Care Center Property Tax Abatement incentivizes property owners to retrofit space to accommodate child care centers for infants and toddlers in the City, especially within child care deserts (defined as census tracts where there are three or more children under five years of age for each available child care slot or where there are no available slots at all). Property owners would be able to recoup all or a portion of construction costs over a five-year period beginning July 2023 through June 2030. Second, the Child Care Business Tax Credit creates a non-refundable tax credit against NYC business income tax liability for businesses that provide free or subsidized child care space for their employees at their place of business. The credit would equal a percentage of Office of Children and Family Services child care market rates, subject to a cap per enrolled child and an overall cap per business. The credits are available for the 2023, 2024 and 2025 tax years.

3 The PTET was enacted in response to the limitation on the federal itemized deduction for state and local taxes (SALT) included in the 2017 federal Tax Cuts and Jobs Act (TCJA). Similar to corporate income taxes, the PTET is imposed on the entire income of pass-through entities, such as S-corporations and partnerships, and, as result, can be fully deducted for federal tax purposes. Members of the entities paying the PTET are authorized to claim a State credit against their personal income taxes for the amount of the PTET paid. In SFY 2021-22, $16.4 billion in PTET was collected which will be offset by the PIT credit in SFY 2022-23.

4 The SFY 2022-23 Executive Budget included a proposal to increase the maximum authorized Rainy Day Reserve Fund balance to an amount equal to 15 percent of State Operating Funds spending. The Enacted Budget increased the maximum authorized balance to 15 percent of estimated General Fund spending (General Fund is a component of the larger State Operating Funds). In SFY 2021-22, a 15 percent maximum balance based on State Operating Funds would have provided for an additional $4.3 billion in Rainy Day Reserve Fund balance authority.

5 The Act defines a lump-sum appropriation as “an item of appropriation with a single related object or purpose, the purpose of which is to fund more than one grantee by a means other than a statutorily prescribed formula, a competitive process, or an allocation pursuant to subdivision five of section 24 of this chapter.” Subdivision five relates to any appropriation added by the Legislature without designating a grantee. Such provision requires that such funds shall be allocated “only pursuant to a plan setting forth an itemized list of grantees with the amount to be received by each, or the methodology for allocating such appropriation. Such plan shall be subject to the approval of the chair of the senate finance committee, the chair of the assembly ways and means committee, and the director of the budget, and thereafter shall be included in a concurrent resolution calling for the expenditure of such monies, which resolution must be approved by a majority vote of all members elected to each house upon a roll call vote.” The 2007 Act prohibited the use of lump-sum appropriations by the Executive for Temporary Assistance for Needy Families, the Environmental Protection Fund, and the Medical Assistance Program.