Even well into the economic recovery, local governments still face challenges, including managing their finances under the property tax levy limit, or “tax cap,” which has been in effect since 2012. Although most local governments are doing well, some struggle with making ends meet.

The Office of the State Comptroller has been monitoring the financial condition of each local government through its Fiscal Stress Monitoring System (FSMS). We have also stepped up efforts to shine a light on the operations of local authorities.

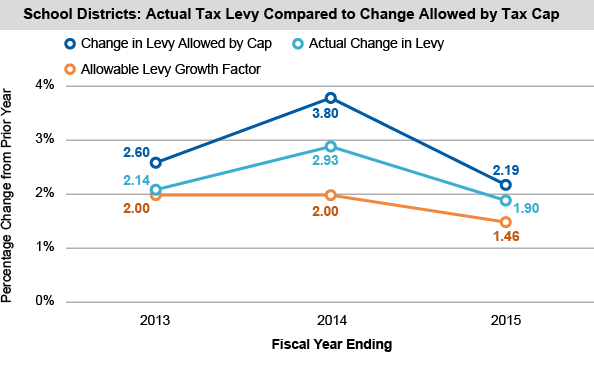

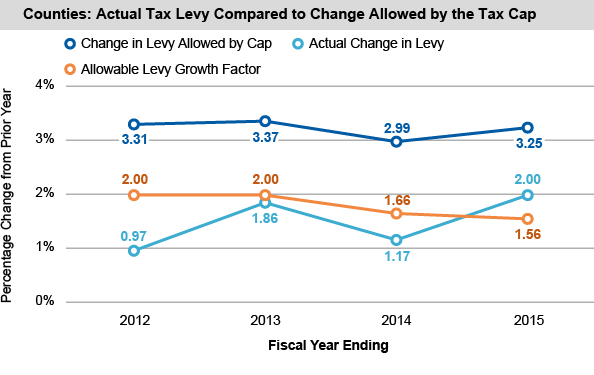

School Districts and Other Local Governments Are Living Within the Tax Cap

The tax cap has applied to schools for three years and counties for four years. Levies, which had been slowing in growth in the years before the tax cap, have stayed well under the limit.

School districts

Since school districts have particularly rigorous requirements for overriding the tax cap, they are less likely to override than other local governments.

- Overall, school district levies stayed within the tax cap in school fiscal years 2012-13, 2013-14 and 2014-15.

- Only 2.8 percent of districts exceeded the tax cap in 2014-15.

Counties

- Overall, levy growth for counties was more than one percentage point less than the tax cap allowed in all four years that it was in effect.

- However, several counties still exceeded the tax cap—over 20 percent of counties in the first three years, declining to 10.5 percent in the fourth year.

Enacted in 2014, the Property Tax Freeze Credit—a tax relief program that reimburses qualifying New York State homeowners for increases in local property taxes on their primary residences—puts even more pressure on local governments and school districts to stay within the tax cap. This is because only taxpayers of municipalities or districts that levy within the tax cap can receive the credit rebate.

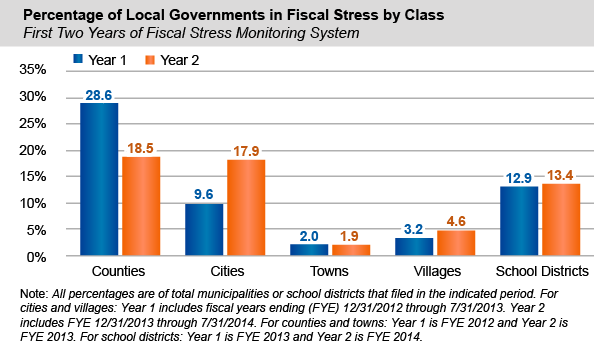

Many Local Governments Are Still Experiencing Fiscal Stress

The Office of the State Comptroller released the second annual FSMS scores for local governments last year. The FSMS gives each local government a fiscal stress score.

The scores inform local and State officials and the general public about the financial issues facing local governments. While most entities had scores that did not put them in any level of fiscal stress, they may still show some risk factors for stress.

The Comptroller’s Office observed some notable changes in how many local governments were in stress between the first and second year of the FSMS.

- The number of counties in fiscal stress dropped by over 10 percentage points from 28.6 percent to 18.5 percent.

- The number of cities in fiscal stress, in contrast, increased by over 8 percentage points from 9.6 percent to 17.9 percent.

- While there was only a small increase in the number of school districts in a stress category, a significant number of schools either moved into or out of stress between the two years.

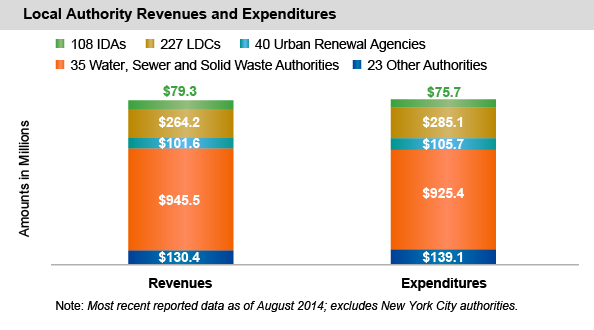

Local Authorities Are Responsible for a Large Amount of Spending and Debt

Local authorities exist to advance the goals of their communities. Because they operate outside many of the controls placed on municipal governments, assessing their effectiveness can prove difficult.

A total of 675 active local authorities exist in New York State, 36 of which are located in New York City. Generally, local authorities must report revenues and expenditures, debt, employment and salary information to the Authorities Budget Office.

Local authorities located outside of New York City reported:

- $1.52 billion in revenues;

- $1.53 billion in expenditures;

- 4,268 employees who were paid $182.3 million in salaries (excluding fringe benefits); and

- $17.7 billion in outstanding debt.

Water, sewer and solid waste authorities as a group represented the largest totals for revenue, expenditure and employment. They reported:

- $945.5 million in revenues;

- $925.4 million in expenditures; and

- 2,640 employees.

Industrial development agencies (IDAs) and local development corporations (LDCs) take the lead in issuing debt. Their $15.1 billion in debt represents 79 percent of debt for all local authorities. Much of the IDA debt is conduit debt—debt that the IDA issues on behalf of a business or other project that the IDA is supporting.

For more information on State and local public authorities, see the public authorities section within this report.