This Google™ translation feature is provided for informational purposes only.

The New York State Office of the State Comptroller's website is provided in English. However, the "Google Translate" option may help you to read it in other languages.

Google Translate™ cannot translate all types of documents, and it may not give you an exact translation all the time. If you rely on information obtained from Google Translate™, you do so at your own risk.

The Office of the State Comptroller does not warrant, promise, assure or guarantee the accuracy of the translations provided. The State of New York, its officers, employees, and/or agents are not liable to you, or to third parties, for damages or losses of any kind arising out of, or in connection with, the use or performance of such information. These include, but are not limited to:

damages or losses caused by reliance upon the accuracy of any such information

damages incurred from the viewing, distributing, or copying of such materials

Because Google Translate™ is intellectual property owned by Google Inc., you must use Google Translate™ in accord with the Google license agreement, which includes potential liability for misuse: Google Terms of Service.

2022 Financial Condition Report

For Fiscal Year Ended March 31, 2022

Taxes

2022 Financial Condition Report For Fiscal Year Ended March 31, 2022

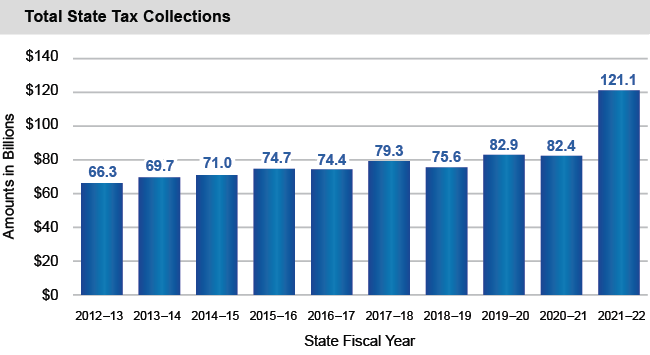

State Tax Collections Increased Significantly in SFY 2021-22 from $82.4 Billion to $121.1 Billion

In SFY 2021-22, reported New York State tax collections increased by 47 percent, primarily reflecting the economic recovery as well as temporary tax rate increases included in the SFY 2021-22 Enacted Budget.

Personal income tax (PIT) collections grew by 28.6 percent due, in part, to the increase in tax rates for those with incomes over $1.1 million (the top tax rate equal to 10.9 percent for incomes over $25 million).

PIT collections also benefited from a 12.4 percent increase in financial industry profits, resulting in an estimated 21 percent increase in securities industry bonuses.

Corporate franchise taxes increased by 46 percent, resulting from higher tax rates in addition to large corporate profit growth.

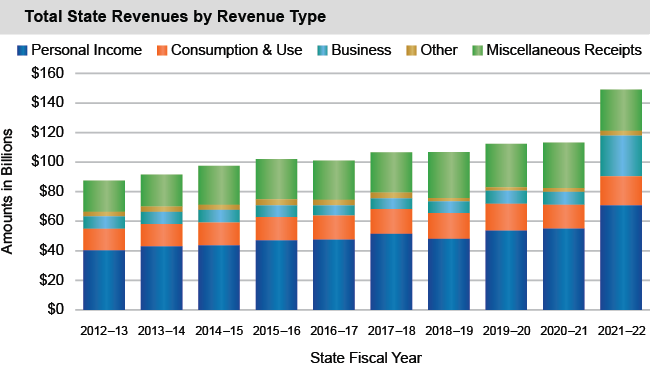

The Pass-Through Entity Tax (PTET) Went into Effect, Inflating Collections

The PTET provides a way for certain taxpayers to avoid the $10,000 limit on federal itemized deductions for state and local taxes (SALT) by imposing the tax on the business entity (S-corporations, LLCs, and partnerships), rather than imposing the PIT on individual members of the business. PTET collections totaled $16.4 billion in SFY 2021-22.

Members of the business entities are authorized to claim a PIT credit for their shares of the PTET paid. Affected taxpayers were not allowed to adjust their tax year 2021 estimated PIT payments for the amount of the tax credit; accordingly, SFY 2020-21 results are distorted due to both PIT and business tax payments having been received, but offsetting PIT credits not having been claimed.

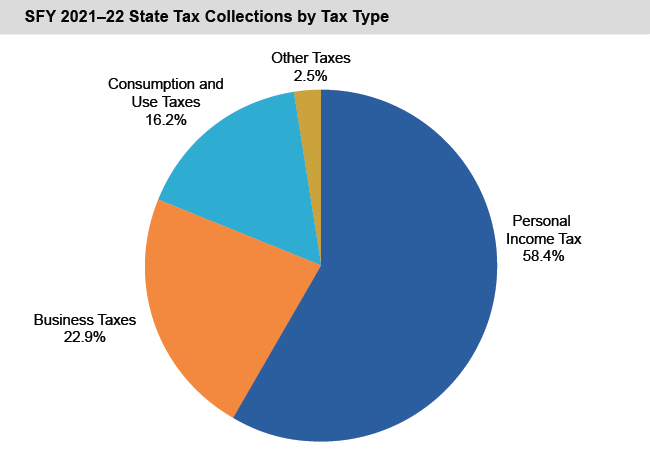

The State Budget Relies Heavily on the Personal Income Tax

Personal income tax collections:

Made up 58.4 percent of New York State’s tax collections in SFY 2021-22.

Were lower than the 67 percent in SFY 2020-21 due to increased business collections relating to the PTET.

Oregon and California had a greater reliance on the personal income tax, 63.2 percent and 59 percent of total tax collections, respectively. Nationwide, over one-third of the states rely more heavily on sales and user taxes.

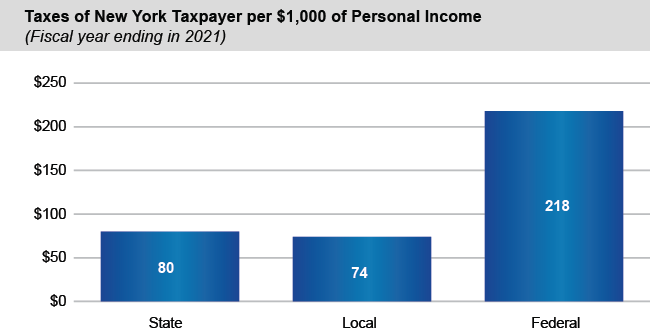

Tax Burden Increases

The combined federal, State, and local tax burden in New York State was $372 per $1,000 of personal income in fiscal years ending in 2021, an increase from $327 in fiscal years ending in 2020.

At the local level, property tax revenues are the largest single tax source overall. Nearly 66 percent of all property taxes in New York are collected by school districts.