The debt burden of a governmental entity creates fixed costs that directly affect its ability to provide current services, as well as its long-term fiscal health. High borrowing levels may:

- Indicate an inability to support current programs with current revenues.

- Force future program reductions, increased taxation or additional future borrowing.

- Limit the capacity to finance capital assets and grants.

New York State Ranks Second Highest in Outstanding Debt Nationwide

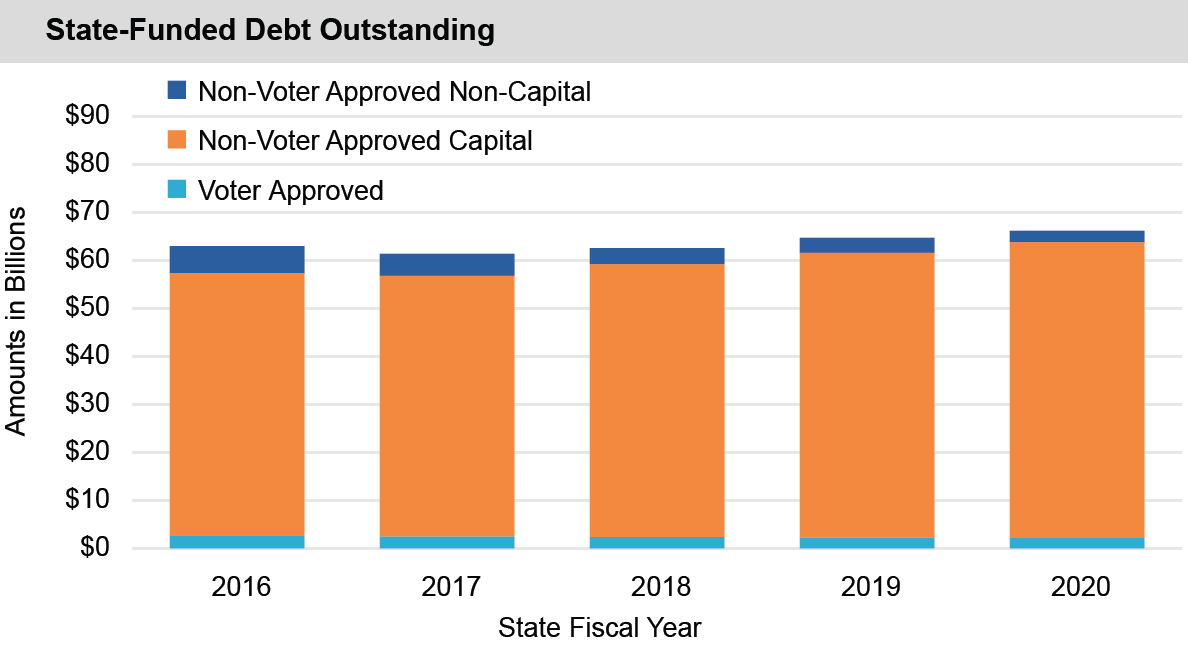

- At the end of State Fiscal Year (SFY) 2019-20, the State reported the following debt levels:

- $2.1 billion of constitutionally-authorized, voter-approved general obligation debt, a decrease of 22.2 percent since SFY 2015-16.

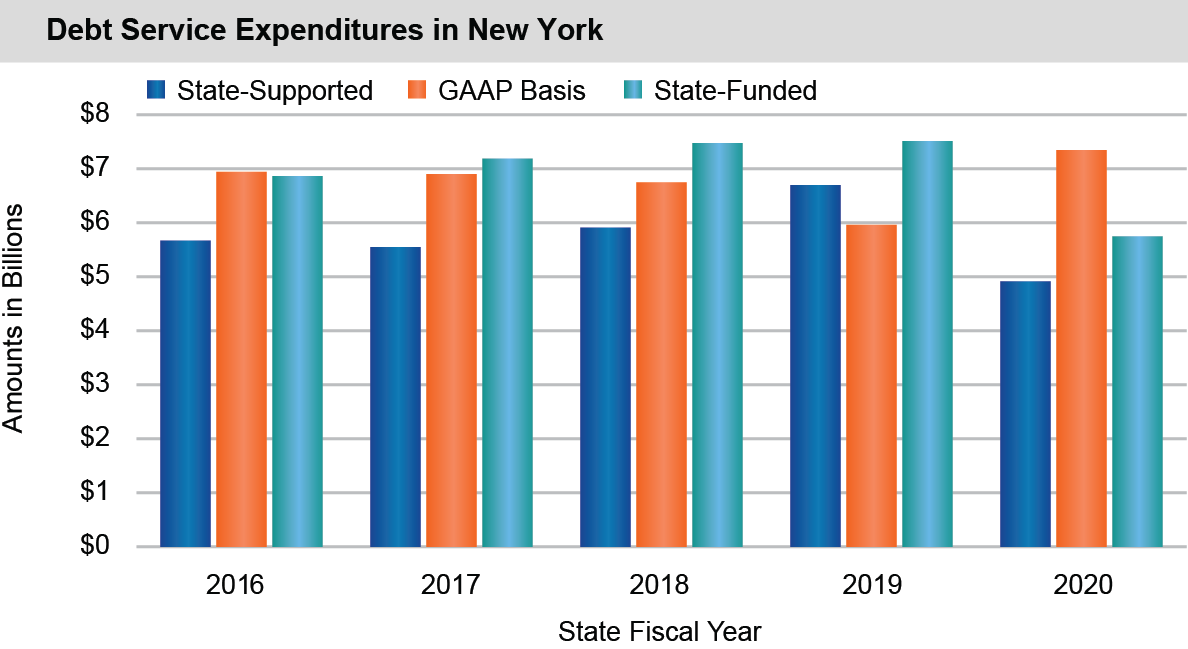

- $54.2 billion of State-Supported debt, an increase of 7.9 percent since SFY 2015-16.

- $60.9 billion of debt reported in accordance with Generally Accepted Accounting Principles (GAAP), an increase of 7.4 percent since SFY 2015-16.

- $66.2 billion of State-Funded debt, an increase of 5.1 percent since SFY 2015-16. This is the State Comptroller’s more comprehensive measure of the State’s debt burden, which includes certain obligations that are not recognized under GAAP or within the measure of State-Supported debt. It recognizes debt where the State makes payments with State resources, directly or indirectly, to a public authority, bank trustee or other municipal issuer. More than 96 percent of State-Funded debt has been issued by public authorities without voter approval.

- In 2019, New York State had the second highest debt burden, behind only California. It was fifth-highest among all states in debt per capita.

- At the end of SFY 2019-20, State-Funded debt outstanding per capita was $3,393. State-Funded debt was equivalent to 4.8 percent of state personal income.

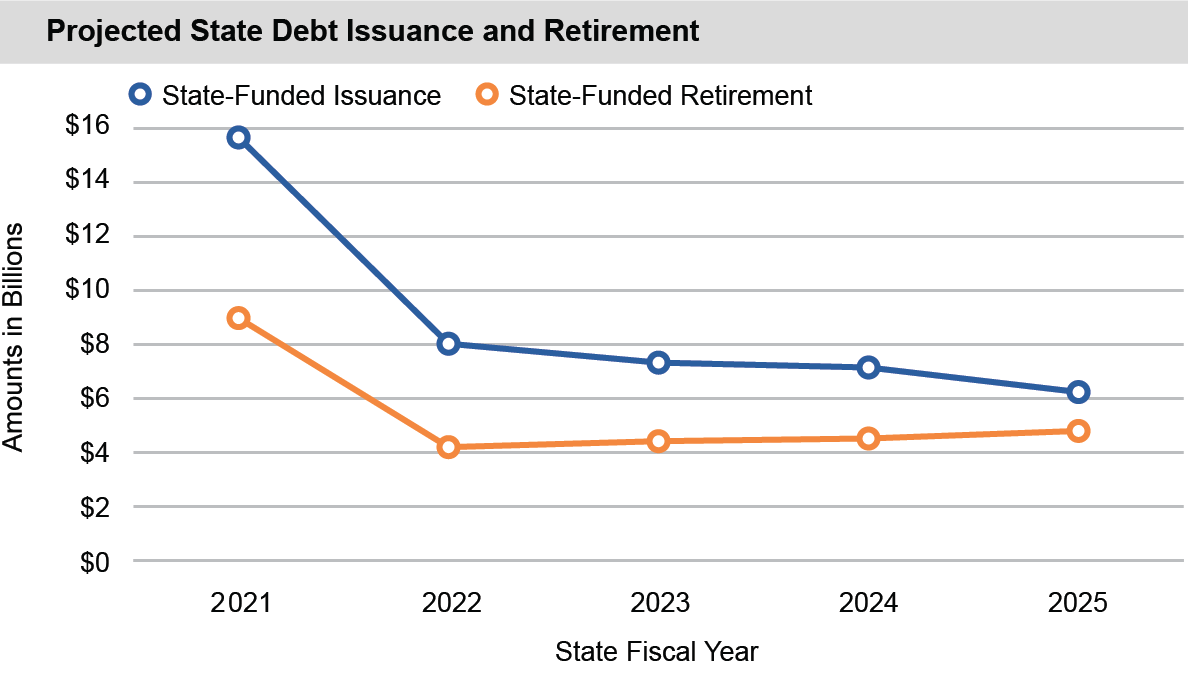

New York State Projects Increasing Debt Levels in Coming Years

- The SFY 2020-21 Enacted Budget Five-Year Capital Program and Financing Plan, as updated by the First Quarterly Update, projects that the State will issue 60.7 percent more debt than it will retire over the next five years, with:*

- $40.2 billion of new issuances of State-Supported debt; and

- $24.4 billion of State-Supported debt retirements.

- The SFY 2020-21 Enacted Budget authorized the issuance of up to $11 billion in borrowings for State cash flow relief. To date, Dormitory Authority of the State of New York has issued $4.4 billion of short-term Personal Income Tax notes, scheduled to be repaid by the end of this fiscal year. It also entered into a $3 billion line of credit—this is available if further support is necessary, although no amounts are expected to be drawn upon. Although not anticipated as of the First Quarterly Update, the legislation permits such borrowings to be rolled into future years and/or refunded by longer-term deficit financings.

- The State projects reduced statutory debt capacity over the next five years, declining to $2.4 billion in SFY 2023-24, primarily as a result of legislated changes. The SFY 2020-21 Enacted Budget amended the Debt Reform Act of 2000 to exclude all State-Supported debt issued in SFY 2020-21 from the State’s debt caps and other limitations, except the maximum term of 30 years. This would exempt an estimated $9.9 billion of debt issuances from the State’s debt caps, not including the $4.4 billion of short-term notes issued for cash flow relief and scheduled to be retired within the current fiscal year. The legislated changes do not reduce the State’s debt obligations or its ability to pay those costs.

- The State’s accumulated deficit financing ($738.8 million in SFY 2019-20) is scheduled to be fully repaid by SFY 2024-25. This includes bonds issued by the New York Local Government Assistance Corporation (LGAC), the Municipal Bond Bank Agency (MBBA) and the Urban Development Corporation. An additional $1.7 billion in debt outstanding is associated with issuances by the Sales Tax Asset Receivable Corporation (STARC) and the sale of Attica Correctional Facility in 1991.

- New York issues State-Supported debt to fund certain capital purpose grants to other entities, which also creates State liabilities without corresponding State assets.

- $466 million in State-Supported debt service otherwise due during SFY 2020-21 was prepaid in SFY 2019-20. Such prepayments typically do not reduce the State’s interest costs, and artificially reduce reported year-over-year growth in both debt service and overall spending levels.

New York State Bond Ratings

At the end of SFY 2019-20, the State’s general obligation bond ratings were assigned as follows.

- AA+ by Fitch Ratings;

- Aa1 by Moody’s Investors Service; and

- AA+ by Standard & Poor’s (S&P) Rating Services.

These ratings are one step below the highest investment grade ratings. Both Moody’s and Fitch have recently assigned a negative outlook to the State’s credit, reflecting the impacts of the COVID-19 crisis on the State’s finances. Ratings can influence interest rates and bond pricing. Higher ratings provide greater confidence to the investment community that the issuer is willing and able to meet the financial commitments of its obligations. The rating agencies have previously cited issuing additional debt for operating purposes as a potential risk factor that may lead to a downgrade of the State’s credit rating.

* Includes debt issued for cash flow relief and scheduled to be retired in SFY 2020-21.